It’s not a sector anymore. It’s more like an asset class.

We Baby Boomers have lived through an industrial revolution. We grew up with cars, diesel engines, and the other major accomplishments of the previous century. But as we grew older, our lives increasingly became driven by technology.

The computer became the device, and the device became a part of our bodies. Whether it is a laptop, mobile phone, or pacemaker, tech has transformed our lives.

Sometimes, I feel like I am the “after” picture in Disney World’s Carousel of Progress, but with a couple of rooms added to that iconic show.

As this evolution transpired, the investment markets took notice. Technology “leaders” used to include companies like IBM IBM and Texas Instruments TXN. Now, those businesses are so mature, I wonder if my kids have even heard of them. Even Microsoft MSFT and Intel INTC, the new tech wizard companies of 20 years ago, are well-entrenched “blue chips.”

Tech stock domination…

Tech stocks are currently the largest sector in the S&P 500. And, at around 22% of the S&P 500 Index, technology stocks in the U.S. have a larger weighting than 5 sectors (Consumer Staples, Utilities, Energy, Real Estate and Basic Materials)…combined!

So, it begs the question. Should tech be treated separately from non-tech stocks when you allocate your portfolio. If you asked me 10 years ago, I would have said no way. Today, I look at it differently.

This is a chart of the S&P 500 technology sector and all of the stocks that are not in the tech sector. This chart goes back to January 26, 2018, the date I believe the bull market essentially ended.

Stocks were certainly capable of going up, as they did for a while. But as you can see, if you extract the tech sector from the S&P 500, the rest of the index has advanced less than 5% in over 28 months. Meanwhile, tech is up more than 47% over that time, despite a pair of large stock market declines.

…OK, not all tech stocks

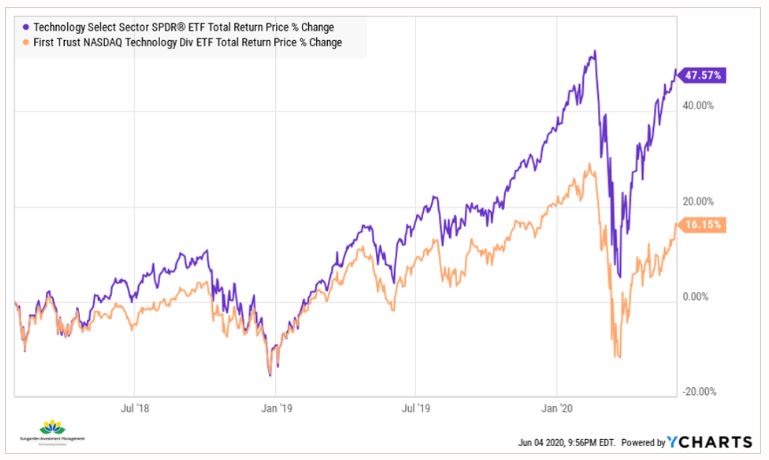

One more piece of visual evidence should help us get a more confident answer. Below is that same tech sector (symbol XLK), but instead of the “non-tech S&P 500,” I compared it to its tech brethren, via an ETF that tracks tech stocks in the Nasdaq NDAQ, but only those that pay a dividend.

Take away those no-yield stocks, and the rest of the group has gained only 1/3 of the total tech sector. That means that the no-yield tech stocks have gained WAY more than 47% in 28 months. Good for them and their shareholders. But, trees don’t grow to the sky, so there’s risk there.

Conclusion: it is not Technology stocks that deserve to be treated as marching to the beat of their own drum, apart from the rest of the market. Instead, it is the big tech stocks that do not pay dividends. For instance, Amazon AMZN, Netflix NFLX, Google GOOGL, Facebook, Tesla TSLA and others do not pay dividends. Apple AAPL, Microsoft, Intel, Cisco and others do.

What to do about this

When you see one segment of the market in its own world, as no-yield tech stocks have been in since the rest of the market essentially topped out more than 2 years ago, you have to look at them as a different beast.

The other time in my career that it really paid off to separate no-yield-tech from the rest of the stock market was back in the 1999-2003 period. That is, the Dot-Com Bubble. Then as now, investors had this love-hate relationship between the 2 groups that at times was a real back-and-forth tussle.

Baby Boomers: heads up!

This distinction is something that every investor who has accumulated some wealth to retire on, and has at least a modest exposure to stock index funds, needs to understand. Otherwise, you risk getting lulled into complacency, thinking that your index funds are “OK.”

Given the years-long, late bull market cycle stampede into no-yield tech stocks, there is a very good chance your portfolio is at risk of being clobbered once this tug of war between this popular market segment pulls back. In the Dot-Com era, that “pullback” was enough to erase more than 1/2 of many mutual fund portfolios.

This is yet another notch in the belt of those who employ an investment approach that looks beyond the tip of the iceberg, so to speak. Dissecting the market into smaller pieces is where I think the real value-added is today in portfolio management. After all, as the pictures above show, the “market” is not what you think it is.