Written by: Brian Levitt | Invesco

For long-term investors, staying out of the market during a period of volatility may hinder your returns.

What if I told you on Christmas Eve 2018 that over the next 15-plus months, ending April 10, 2020, the US equity market, as represented by the S&P 500 Index, would be up 18%?1 If you’re like me, then you likely would have rejoiced, especially following a year like 2018, in which the uncertainty of US trade policy and tighter US monetary policy led to a rare negative-return year in the broad market.2 However, I would have been hard pressed to imagine, in that scenario, money market assets having increased by 50% over that period to $4.5 trillion.3

I understand that this has played out differently than we expected, the 18% gain in US equities notwithstanding. The uncertainty of the coronavirus outbreak persists. Perhaps the new baseline assumptions that aggressive monetary and fiscal support can bridge us through this period while we await new COVID-19 treatment and rapid testing are too optimistic. Perhaps more equity volatility and another drawdown are on the horizon.

Still, $1.5 trillion in new money market assets is unsettling. For perspective, that’s enough money to buy everyone in San Francisco an apartment, and still have $500,000,000,000 left over.4 That’s enough to pay a year’s salary for 30 million teachers.5 I digress. The flow of dollars into cash equivalents will likely prove reflective, once again, of investors making imperfect decisions at inopportune times. I’ll take some solace in it as a good intermediate-term contrarian indicator for markets but lament that many investors just missed the best week in the US equity market since 1974 and the 7 of the best 30 days since 1995.6 I’d be remiss if I didn’t once again include the chart below detailing the ruinous impact of missing the market’s best days.

Figure 1: Missing the best market days can be detrimental and they almost always happen during bear markets

The fear of missing out is likely being overwhelmed by investors being conditioned for rallies that provide some short-term relief and are then followed by markets re-testing lower levels. Truth be told, a retest of the March 23, 2020 low would have investors posting slightly negative returns since Christmas Eve 2018. A retesting of lows isn’t a prediction, but a possibility, nonetheless. The flight to cash, in that scenario, would likely persist. For example, during the global financial crisis, money market assets, according to the Investment Company Institute, ultimately doubled before peaking in the first quarter of 2019, not surprisingly in time for equities to begin a decade-long ascent.

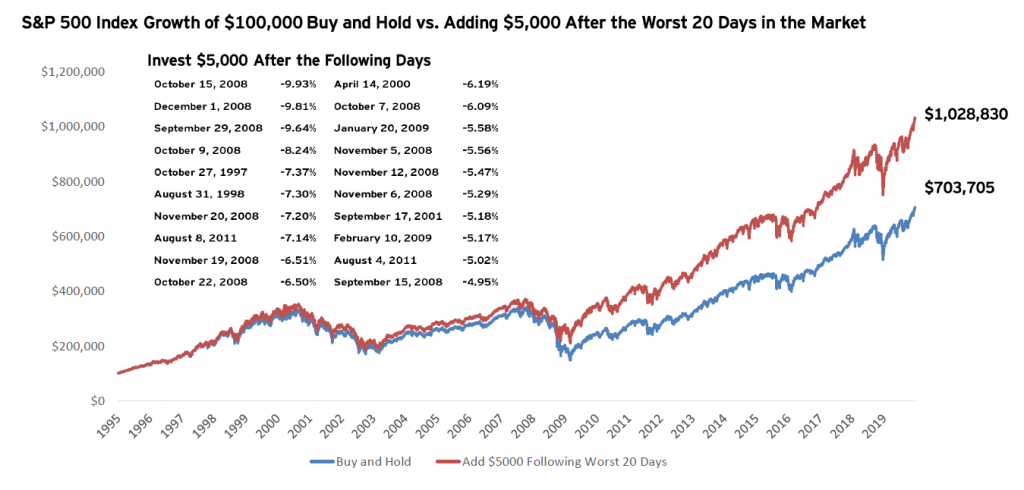

Reflecting on what you should have done in 2008 and 2009 may provide guidance for how investors should be responding now. What if investors, instead of fleeing to cash during the tumultuous times, instead invested more money following each of the worst days in the market? Figure 2 below demonstrates the experiences of two hypothetical investors. Both invested $100,000 in the market in 1995. One investor never added to the portfolio. The other investor added $5,000 to the portfolio after each of the 20 worst days in the market, 13 of which happened in 2008 and 2009. Adding $5,000 to the portfolio, following each of the worst 20 days in the market, enabled the second investor to have $300,000 more dollars by the end of 2019 than the investor who never added to the portfolio.7 There’s a Baron Rothschild quote that applies, but far too insensitive for the times to publish.

Figure 2: Historically, adding to the portfolio after the worst days has been beneficial

The point is that the next weeks will likely bring more uncertainty and persistent volatility in markets. Our instincts will likely be to add to the $4.5 trillion already sitting in money markets. History reminds us that being in the markets for the best days, and even adding to portfolios following the worst days, has been the better approach.

1 Source: Bloomberg and Standard & Poor’s, as of 4/10/20

2 Source: Bloomberg, as of 12/31/19

3 Source: Investment Company Institute, as of 4/10/20

4 Source: US Census Bureau, Realtor.com, as of 4/10/20

5 Source: Bureau of Labor Statistics, as of 12/31/19

6 Source: Bloomberg and Standard & Poor’s, as of 4/10/20. As represented by the S&P 500 Index

7 Source: Bloomberg and Standard & Poor’s, as of 4/10/20. As represented by the S&P 500 Index