As mentioned I’ve just attended #Money2020Europe where 4,000 folks gathered to listen to great speakers like me. Unfortunately, I didn’t get long to stay at the show for various reasons, but did pick up a magazine about Copenhagen as a FinTech hub.1 Everywhere wants to be a FinTech hub, now that the scene is so active and key. Not everywhere will be a hub, as only so many places can offer the right capabilities. For example, it was interesting talking with Jon Weiner the co-founder of Money2020, who lives in Lisbon and was telling me about their leading tech capabilities. Do they have a FinTech centre in Lisbon? I asked, as I’d never heard of one. No, Jon said. Unsurprising as Lisbon isn’t really a Global Financial Centre.So you would expect the world’s global financial centres to encourage and nurture FinTech. In the latest Z/Yen Global Financial Centres Index (issue #19, March 2016 ), London, New York, Singapore, Hong Kong and Tokyo comprise the top 5. Intriguingly, the first three are very actively building their FinTech capabilities but, having been in Hong Kong and Tokyo recently, I know they are more challenged. For example, a colleague at Bank of Tokyo-Mitsubishi presented this slide in the FinTech forum I attended there:  This is Japan’s FinTech scene and it’s tiny, compared with London and New York.KPMG’s Pulse of FinTech 2015 report illustrates the challenge further, showing that US FinTech leads the world. Of the $13.8 billion invested by Venture Capital firms in FinTech in 2015, $7.39 billion went into US start-ups, compared with $4.5 billion into Asian firms and just $1.5 billion in European organisations.

This is Japan’s FinTech scene and it’s tiny, compared with London and New York.KPMG’s Pulse of FinTech 2015 report illustrates the challenge further, showing that US FinTech leads the world. Of the $13.8 billion invested by Venture Capital firms in FinTech in 2015, $7.39 billion went into US start-ups, compared with $4.5 billion into Asian firms and just $1.5 billion in European organisations.

The 10 largest FinTech funding rounds in America, 2015

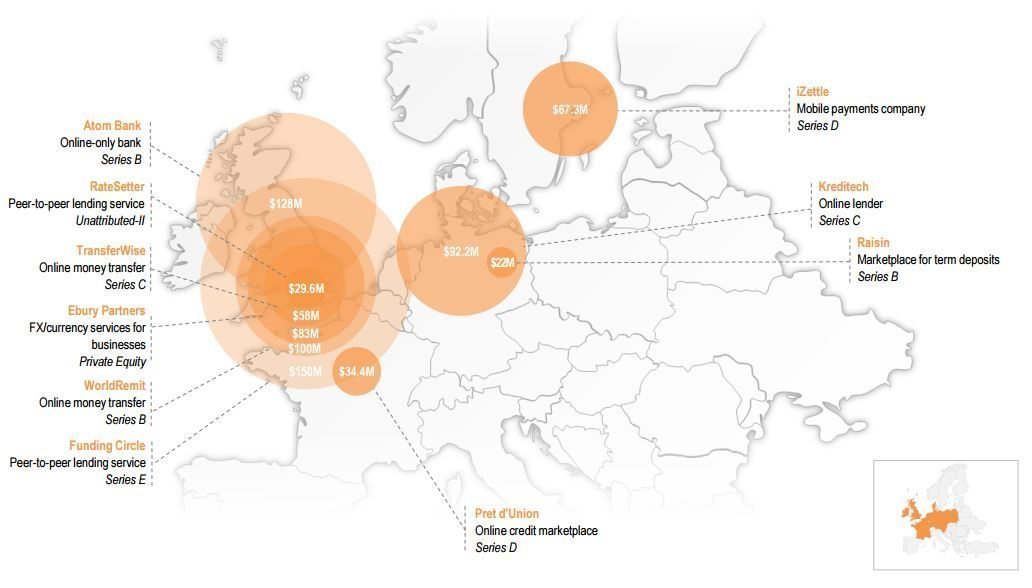

The 10 largest FinTech funding rounds in Europe, 2015

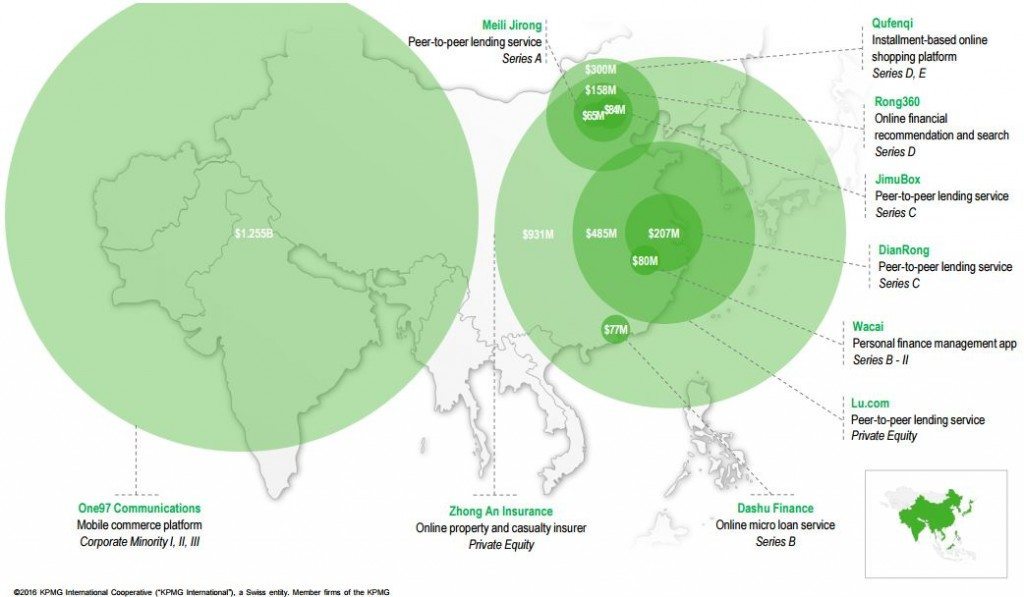

The 10 largest FinTech funding rounds in Asia, 2015

So what does it take to truly become a FinTech hub?Well, going back to Copenhagen, my friends at CFIR commissioned Oxford Research and Rainmaking Innovation to find out the answer. The resulting research report concludes that there are six key factors for becoming a FinTech hub:

So what does it take to truly become a FinTech hub?Well, going back to Copenhagen, my friends at CFIR commissioned Oxford Research and Rainmaking Innovation to find out the answer. The resulting research report concludes that there are six key factors for becoming a FinTech hub: