Written by: The Fixed Income Team | Putnam Investments

- A U.S. recession is now all but certain as social distancing takes a toll on sentiment and businesses.

- The Fed's liquidity lifelines to credit markets should stabilize the financial system and the economy.

- We see potentially attractive opportunities, including securitized debt, when markets stabilize.

An extremely sharp global downturn is unfolding as the coronavirus pandemic takes a toll on economic activity and sentiment. The virus and the collapse in oil prices have unnerved investors and sent financial markets into a tailspin. This escalating economic crisis elicited unprecedented measures from policy makers. The Federal Reserve slashed interest rates to near zero, extended terms on emergency loans to banks, relaunched a financial-crisis-era commercial paper tool, and extended other lifelines across the bond market. Still, the U.S. economy is heading into a recession — abruptly ending an 11-year expansion — as lockdowns hurt work, businesses, and travel.

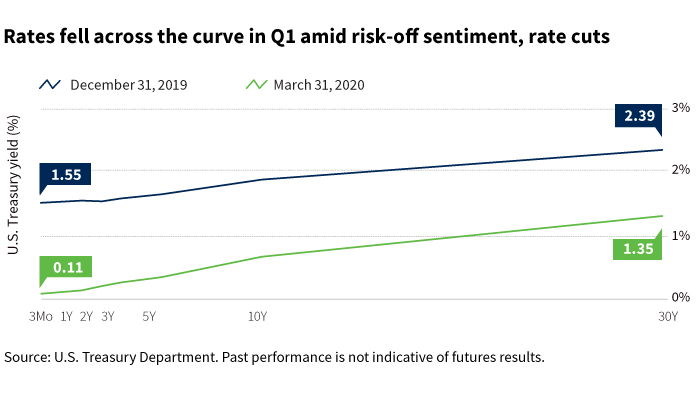

The global scramble for cash is also putting immense pressure on U.S. Treasuries and other credit markets. Developed-market government-bond yields declined, credit spreads widened, and the yield on the benchmark 10-year Treasury note set a record low on March 9. The Treasury yield curve has also steepened slightly, as the gap (or spread) between two- and 10-year yields touched its widest point in two years in March. A stampede into dollars — widely considered a safe-haven currency — has pushed up the value of the dollar against the majority of its global counterparts. Elsewhere, the European Central Bank (ECB) kept rates unchanged but expanded its asset purchases to include a new €750 billion bond-buying program. Central banks across Asia and other regions also announced emergency stimulus measures.

The market for corporate bonds — both high-yield and investment-grade credit — also collapsed during the quarter amid the global sell-off in equities. The spreads on investment-grade bonds, or the risk premiums investors demand to hold these securities rather than U.S. Treasuries, widened to levels not seen since the financial crisis. The Bloomberg Barclays U.S. Aggregate Bond Index rose 3.15% during the third quarter. Despite the dislocations in the market, we have a favorable long-term outlook on investment-grade corporate bonds and some sectors within mortgage-backed securities. Within prepayment-sensitive areas of the market, we believe these securities will be less sensitive to refinancing risk in a low-interest-rate environment.

U.S. economy set to contract

The COVID-19 outbreak and the collapse in oil prices have pushed the U.S. economy into unchartered territory. Meanwhile, "social distancing" has dealt a serious blow to demand. The Fed said in mid-March that the effects of the coronavirus will "weigh on economic activity in the near term" and pose "risks to the economic outlook." An estimated 90% of the U.S. population is now under some kind of "stay at home" measure. Restrictions on economic activity and travel have broadened, companies have laid off workers, consumers have curtailed spending, and some smaller businesses are struggling to service their debt. In addition, U.S. employers shed more jobs in March than in any month since March 2009. The unemployment rate rose to 4.4% from 3.5% in February, according to the Labor Department.

The escalating economic crisis elicited unprecedented measures from policy makers. The President and Congress approved a historic $2 trillion stimulus package intended to rescue the economy reeling from policies to stop the spread of the coronavirus. But it will take quite some time for economic activity to move back to its levels before the COVID-19 pandemic. Demand will remain weak for as long as "social distancing" remains in place. We could see a relaxation of restrictions in late May. We believe a period of contraction is inevitable; first-quarter GDP will decline, and the second quarter will show a larger contraction. Overall, however, the economy is contracting sharply; it's not grinding to a halt, but the brakes are on.

The Fed's war chest

On March 15, the Fed cut interest rates to a target range of 0% to 0.25% and unveiled a sweeping set of programs — including plans to snap up huge amounts of government and mortgage-backed debt — in an effort to backstop the economy. The measures to improve liquidity include the Commercial Paper Funding Facility, the Money Market Mutual Fund Liquidity Facility, and the Secondary Market Corporate Credit Facility. The Fed also pledged to make unlimited asset purchases. Policy makers aim to protect the financial system and insulate the broader U.S. economy. The size of the Fed's war chest, and its flexibility in deploying its authority, give us some comfort that the stresses we saw in the Treasury markets and at the front end of curves have abated.

Fed chair Jerome Powell said on March 15 that the central bank is prepared to use its "full range of tools to support the flow of credit" to households and businesses and thereby promote its maximum employment and price stability. We expect that a temporary burst of volatility will be met with a rapid response. Given the overwhelming policy response, we think Treasury yields will remain low across the curve for an extended period. The 10-year Treasury yield plunged to an all-time low of 0.31% on March 9 and ended the quarter at 0.67%, after starting the year at 1.88%. The 2-year note yield tumbled to around 0.25% at quarter-end.

ECB comes to the rescue

The ECB is not out of ammunition, but it doesn't have a lot of measures remaining to fight the economic fallout from the coronavirus. In March, the ECB launched an emergency bond-buying program worth €750 billion and also scrapped the cap on how many bonds it can buy from any single eurozone country. The bank left its key interest rate unchanged at –0.5%. Other countries in the region, including Spain and France, have announced economic stimulus packages. Germany, Europe's largest economy, unveiled a €750 billion fiscal package, including a €500 billion bailout fund for industries. Italy, the eurozone's third-largest economy, is the epicenter of the pandemic in Europe. A recession in Europe seems inevitable, and growth for the year will be negative.

In the United Kingdom, the Bank of England and Prime Minister Boris Johnson's government stepped up their responses to the pandemic. The government will pay a large part of workers' salaries as long as companies keep their employees, mirroring policies adopted by other European states. The BoE cut interest rates and will undertake large-scale asset purchases. The consequent dramatically higher borrowing requirement has not had much of an impact on government bonds (gilts) even though the country will need to attract global capital to finance itself.

China to rebound slowly

China, the place where the outbreak started, is now beginning the process of returning to something more like normal. Manufacturing activity rebounded in March, signaling that the world's second-largest economy is restarting from the slump caused by the virus. The purchasing managers' index rose to 52.0 in March from a record low of 35.7 in February. Readings above 50 signal improving conditions. The services and construction sectors, however, remain in contraction. So, there is uncertainty about the dimensions of the economic drop and about the current and prospective pace of recovery. The outlook will depend on how fast domestic and external demand can rebound. We believe a slow and modest recovery is underway for the year.

With the economy expected to shrink in the first quarter, China plans to unveil a stimulus package to stabilize the economy. The government plans to increase its fiscal deficit, issue special sovereign debt, and allow local governments to sell more infrastructure bonds, according to local press reports. Details remain scarce, pending China's 2020 budget. The central bank in late March cut the interest rate it charges on loans to banks by the biggest amount since 2015. The People's Bank of China reduced the rate on 7-day reverse repurchase agreements to 2.2% from 2.4%.

Related: “Courage! We Have Been Here Before”