Written by: Christopher M. Brigati | AAM

Prior to the outbreak of the coronavirus, the domestic economy appeared to be on solid footing with reasonable growth prospects and no inflation in sight (as measured by the Fed)...

Since that time, economic impacts regarding the spread of the virus have taken center stage as interruptions to supply chains and global travel have been felt to varying degrees around the globe. The rates markets were quicker to respond; and both the 30-year and 10-year U.S. Treasury (UST) set new historic low yields within the past several days. The effect upon equity markets were finally felt, albeit much later than the fixed-income markets.

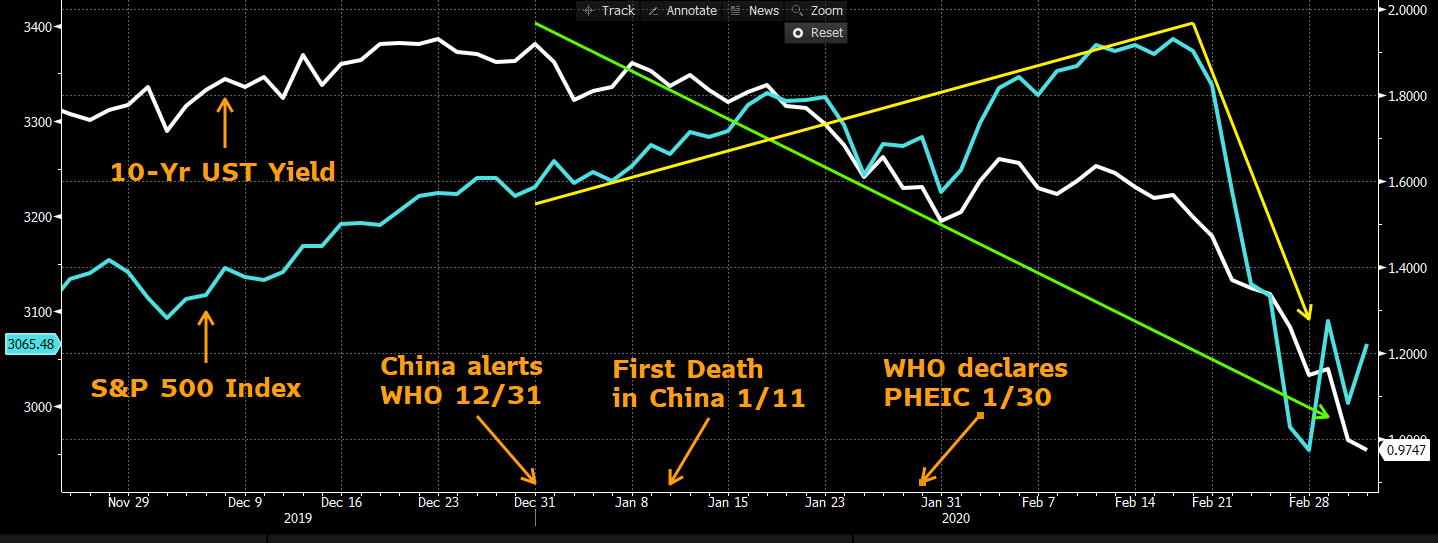

It is impossible to draw direct singular correlations between the coronavirus news and capital market movements given the multi-variate influences upon the markets. We can, however, infer there is a reasonable level of correlation, especially directionally. Initial news about the outbreak starting in Wuhan China broke in late December 2019. The news was not nearly as widespread as it became in late January, but it did build throughout the month at a steady pace, especially after the first attributable death. On January 30, the World Health Organization (WHO) declared the outbreak to be a Public Health Emergency of International Concern (PHEIC). Interest rates and equities reacted differently over the past two months despite the increased concerns about the virus as time progressed. The below chart highlights the movement in the 10-year UST and the S&P 500 Index over this time period.

Source: Bloomberg

As one can see, the 10-year UST demonstrated a relatively steady decline in rates (green arrow), as would be expected for investors seeking the safety of the benchmark UST debt during times of turmoil. Contrarily, the S&P 500 Index continued to climb to record highs, albeit with a temporary blip on the way higher, only to finally experience a rapid and significant sell-off (yellow arrow) well after initial news of the outbreak was announced.

Since interest rates appear to be more responsive to concerns about the virus, as opposed to the slower response from the equity markets, this prompted one investor to ask an age-old question: “Is the bond market smarter than the stock market?”

Being a career-long professional in the fixed income markets, my immediate response should have been obvious. I replied with an emphatic, “Yes!” I expanded upon the answer with, “Additionally, bond-market professionals are also smarter, better looking, funnier, all around better people…and did I mention more humble?”

In reality, the answer is much more nuanced. Fixed income investors generally have more wealth and the market is more significantly influenced by professional investors. Additionally, such investors typically have a longer time horizon, and are more concerned with wealth preservation and value-investing as opposed to growth. The equity market, on the other hand, has a plethora of individual investors with arguably shorter investing timelines, a growth-oriented approach and are more fickle about the market in general.

In general, the number one concern for fixed income investors is potential increases in inflation. Furthermore, the absolute level of inflation (low vs high) weighs into their participation in the markets. Equity investors focus upon corporate earnings and business growth. The economy can be in a low inflation, steady growth environment – as has been the case for the past decade – allowing both markets to move steadily higher in price at the same time. But, the driving influences upon investors are markedly different for each market.

So, why was the equity market slower to react to the coronavirus concerns? As mentioned above, equity market participants typically have a different investing modus operandi and FOMO (fear of missing out) investing, along with no glaring indication that the global economy would decline as a result of supply chain interruptions were obvious. More recently, economic slowdown concerns began to increase as news from corporate boardrooms indicated the complex formula regarding their business growth, earnings potential and global operation inputs were being compromised. Once these concerns became a reality, the equity markets fell sharply as investors fled in droves. The “more stoic and stately” fixed income markets, appear to have more steadily and consistently priced in the “potential” for the global economic impacts which has only more recently become accepted by the equity markets. Thus, interest rates tracked lower, as the safe haven of U.S. Treasury debt was sought.

I stand by the initial answer to the question, especially the expanded description of fixed income professionals…because, I can. I acknowledge, however, the unique drivers for investors in each market influence how they react to any economic stimuli. Perhaps it’s more fair to suggest that the fixed income markets demonstrate a more patient approach akin to a seasoned, wise elder as compared to the more reactionary, excitable response one might expect from an adolescent with a different risk/reward profile. What can we learn from this recent market activity? Perhaps investors can take away, that the fixed income markets have the potential to provide earlier insight into the potential effects of global influences upon the economies of the world, while equity markets might offer emphatic confirmation. The timing of these responses is crucial to making intelligent investing decisions for investors in both markets.

Related: The Coronavirus, Irrationality and the Uptick Rule

DISCLOSURE:The views and opinions expressed in this article are those of the contributor, and do not represent the views of Advisorpedia. Readers should not consider statements made by the contributor as formal recommendations and should consult their financial advisor before making any investment decisions. To read our full disclosure, please click here.