Written by: Matt Lloyd | Advisor Asset Management

Of the most cringeworthy phrases to announce publicly, “This time it’s different” may be at the top…barely beating out the “It’s not you, it’s me” and “In my day….” In economic and capital market terms, the current expansion has been riddled with many unique traits that are normally not seen during normal business cycles. We have discussed the anomalies and abnormalities in the past, however, with the recent market pressure due primarily to the coronavirus, it is good to look at those again and also some new metrics that are standing out.

The coronavirus has all the makings of a rehashed Hollywood story from the unknown origins and potential cases for increased fatalities and economic interference. If one compares it to SARS or other past epidemics, one is accused of not understanding the potential devastation this can cause. Stating that this is going to be the one of the worst pandemics witnessed in modern history opens one up to fear mongering. The chasm between these two scenarios leaves a lot of broad conclusions that only affirms the diverging opinions whether the markets are resilient or apathetic.

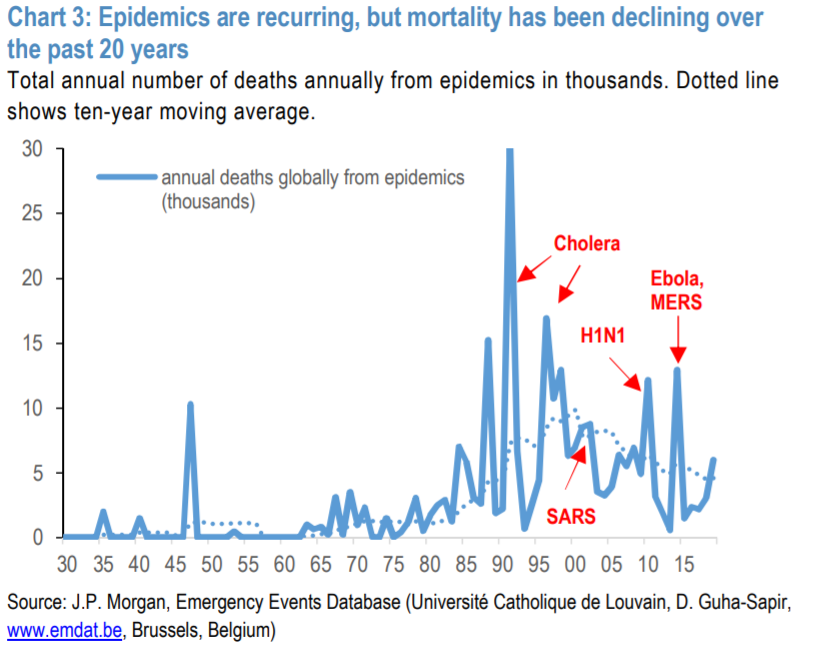

For argument’s sake, looking at past epidemics, we see patterns and can come to a general conclusion. JP Morgan shows this graphically over the last 90 years and measures total deaths from these epidemics. One point of note is that traditionally the two areas of the market that get hurt the worst is oil/energy and China. So far oil and energy has entered a bear market as a result from the virus while China has seen a slight correction of 1.65% year to date.

Though we have seen these patterns repeat itself, it is equally as hard not to assume a worst-case scenario and continuously stay on the sidelines. The more difficult the buy, the more opportunity that typically exists.

While many are saying central banks will help stop this by injecting liquidity and lowering rates, one must wonder how much ammunition they have as well as ask, “Will monetary stimulus really curb the economic slowdown from this virus?” What many are forgetting is that fiscal stimulus at this point would be a more impactful use of funds, not to mention that some of the slowdown in the economic numbers often gets recouped later as the virus is contained. One area that probably won’t recover what was lost was the airline usage and travel that due to the Chinese New Year when expectations were for 400 million to travel in China prior to the virus. In contrast, Thanksgiving in America generates roughly 55 million travelers.

The economic impact on China has been profound and will require a large dose of stimulus to reignite their economic engine. The good news is they have quite a bit of liquidity and more room than the other major central banks to a more accommodative stance. Here are some basic liquidity improvements to liquidity and where they may occur:

- - China currently has $3.1 trillion in currency reserves, or 26% of the $11.8 trillion that exists worldwide.

- - China’s M2 money supply has increased 8.4% year over year, however, that is nearly half of the average over the last 25 years when the average growth was 15.7%.

- - Ample room to increase this form of liquidity. This also could prove to be somewhat inflationary should the traction take place in consumption as we expect.

- - The Required Reserve Ratio for major banks stands at 12.50%, well off its high in 2011 when it stood at 21.50%. However, it is still off the all-time lows of 6.0%.

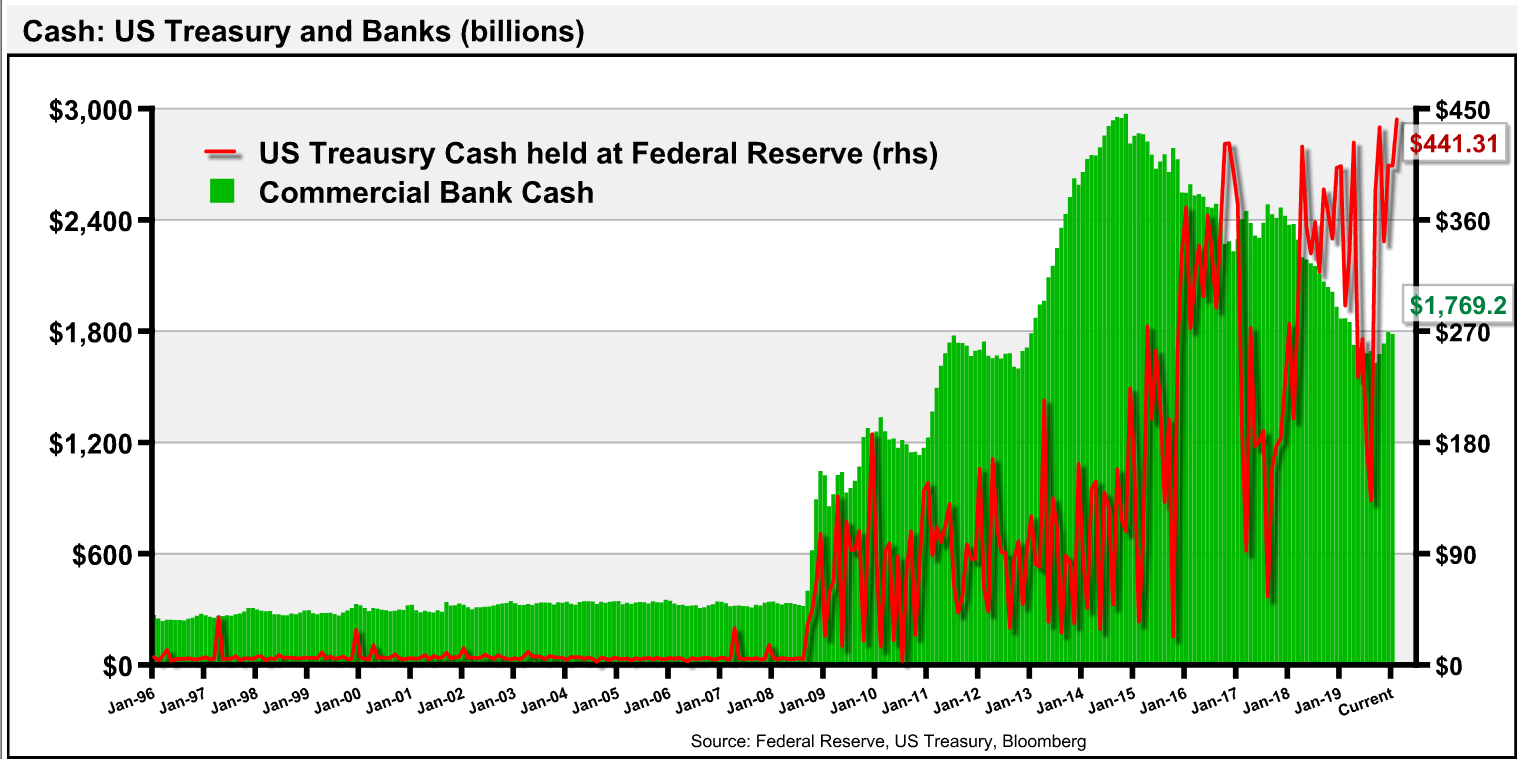

Closer to home and the ability to fund this fiscal stimulus, consider that the U.S. Treasury is currently holding its largest amount of cash at the Federal Reserve in history. They currently hold $441 billion.

One other area where excess liquidity exists is the amount of cash held by commercial banks. Though off its high of nearly $3.0 trillion, they still hold $1.7 trillion in cash and is one of the multiple reasons why we consider banks and financials in general to be one of the better places to be invested.

The risk-off mentality has been one of the most pronounced herding moves seen since the aggressive allocation was done for Y2K and even going back to tulips. Consider the difference of global equity fund flows and global bond flows since 2007.

Source: JP Morgan | Past performance is not indicative of future results.

There has been a net inflow of $2.5 trillion into global bond funds versus global equity funds. In 2019, we had the largest difference with nearly $1.03 trillion going to traditional risk-off bonds versus equities. That equates to 40% of the total difference over 13 years occurred last year when negative interest rates were at its highest level ever.

This has moved Treasuries to near or at their all-time lows. Currently the 10-year Treasury stands at 1.33% and the 30-year at 1.80%. For technicians it seems the 10-year may be setting a triple bottom. For those who enjoy history, the 10-year Treasury set a low on July 2016 at 1.38% only to see rates rise to 2.60% five months later in December 2016. The price in the principal over that timeframe would see a decline of over 10% It may be that the tune the risk-off crowd is playing may conclude to take profits in some of the most conservative of assets and deploy into the area where we see the least amount of favor (value, financials, commodities, Emerging Markets, etc.).

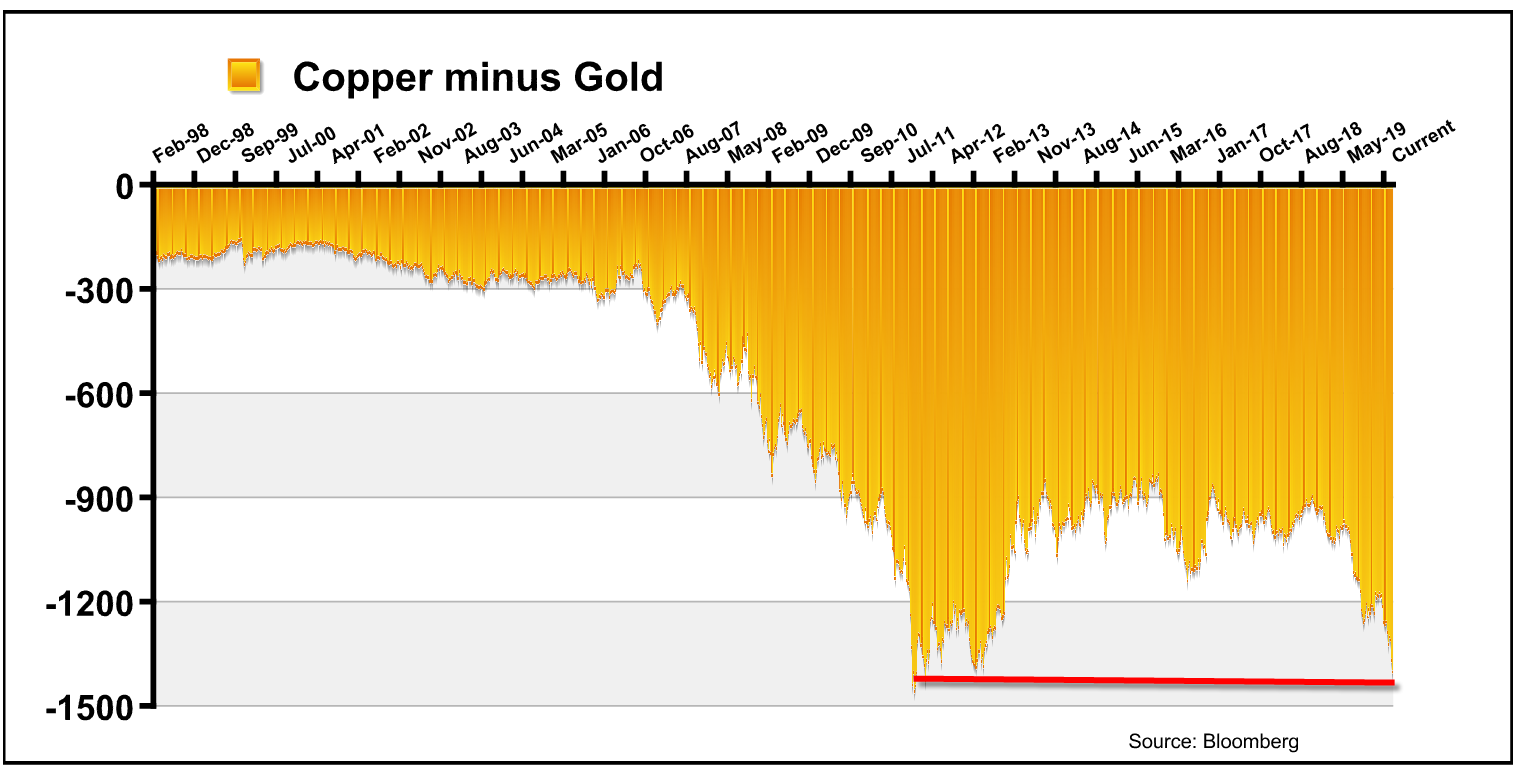

The spillover to risk off has moved to more gold purchases. Consider the measurement of copper minus gold which measures the perception of a healthy economy (copper) and a concern about inflation/economic slowdown/fiat currency troubles (gold). The spread of gold’s outperformance relative to copper’s selling pressure has brought us to levels not seen since September 2011.

This is a very poignant move as what happened to the equity markets over the next two years.

|

|

S&P 500 |

S&P Growth Index |

S&P Value Index |

|

1 Year |

18.60% |

19.05% |

18.04% |

|

2 Year (Total Return) |

40.79% |

37.29% |

44.88% |

Source: Bloomberg | Past performance is not indicative of future results.

If history rhymes, we may be up for a bit more volatility based on some uncertainties and increased infections but be prepared to put money to work. Perhaps the phrase we should continue to use like a Stuart Smalley daily affirmation is to, “Buy on the cannons and sell on the trumpets….” There’s not a lot a lot of music being played right now but the band may be getting ready to play an encore.

DISCLOSURE:The views and opinions expressed in this article are those of the contributor, and do not represent the views of Advisorpedia. Readers should not consider statements made by the contributor as formal recommendations and should consult their financial advisor before making any investment decisions. To read our full disclosure, please click here.