Written by: Guild Investment Management

Global stock markets reacted to the ongoing COVID-19 scare with unusual volatility last week, with U.S. stocks shedding about $4 trillion in value over six bruising sessions.

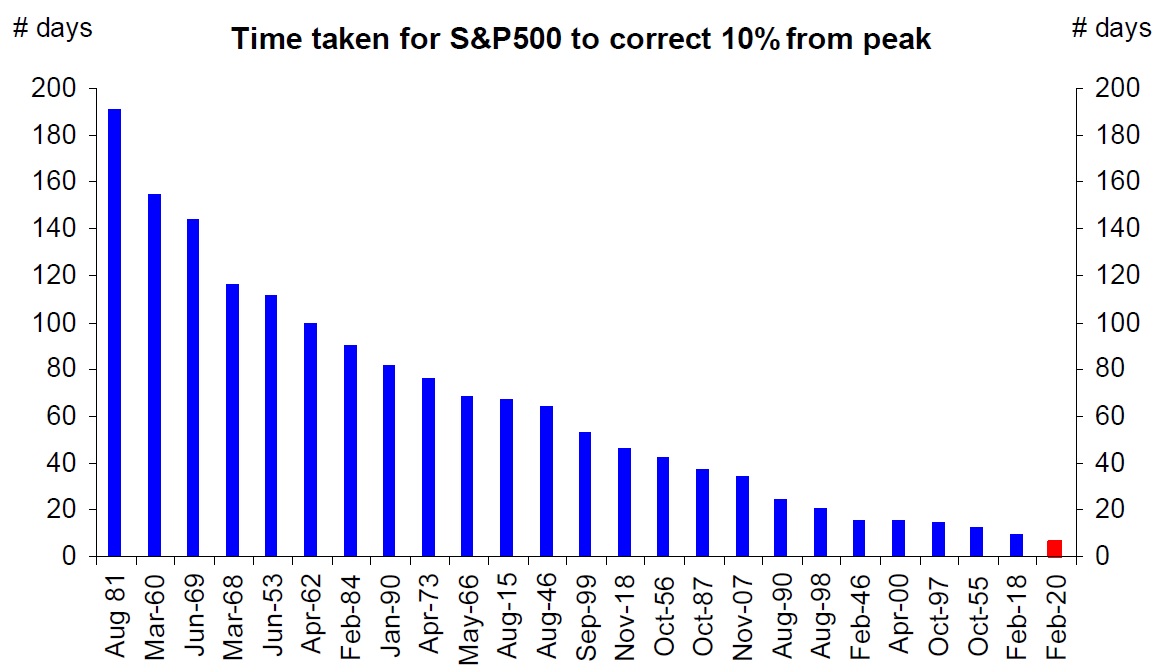

The decline marked the fastest 10% correction from the peak in S&P 500 history (during 1987, the peak was in August, months before Black Friday that October). As we write, volatility — both up and down — has continued, with U.S. markets recovering substantially. We believe that this market decline was more reactive than rational. If it wasn’t rational, then the rational thing to do is to try to understand what happened so that we can determine if it indicated that the existing trend was pausing — or if it indicated that a new trend was emerging. That’s where our attention has been focused.

So was it rational for global stock markets to slough off $6 trillion in value over the course of a single week? Once we figure that out, we’ll explain why the market’s irrationality might have had to do with a trading rule that got canned in 2007 — the “uptick rule.”

COVID-19: What’s Really Going On

Since at any given point, the valuation of stocks depends on the market’s view of the future trajectory of earnings, the answer to that question depends on the answer to the worries at the top of everyone’s mind about the impact of COVID-19. Our first step, then, has been to stay abreast of the best data we can find on the virus, from the most neutral sources. Most mainstream media, no matter their political slant, have a built-in tendency to sensationalize current events, since they are desperately seeking survival in an “attention economy,” and fear (unfortunately) drives attention.

Here are some data points that we’ve been considering.

For perspective, there is another virus which has already infected 19 million Americans, hospitalized 180,000, and killed 10,000 — this year’s flu. The fact that COVID-19 is new seems to have created a level of fear that doesn’t accompany the boring things we already live with every year.

Data on the mortality rate for COVID-19 are in flux. Still, we noted that at a Beijing press conference, Chinese health officials put the mortality rate within China, but outside Wuhan province at 0.7%. The higher mortality rate in Wuhan is believed to represent the early dynamics of the outbreak, when it remained unknown, cases developed longer before patients sought treatment, and palliative care procedures were not established. (Patients with already-compromised lung function due to pollution, tobacco use, etc., were also hit harder.) In South Korea, the mortality rate has been about 0.5%. Those levels would put COVID-19 at the level of a severe influenza epidemic. Again, though, it will be some time before a full picture of the virus’ lethality becomes clear; numbers are different in other countries, such as Iran and Italy.

In some other respects, such as the higher risk faced by elderly and immunocompromised patients, the severity of COVID-19 is also likely similar to a bad flu season (but we add, not a catastrophic flu pandemic like that of 1918, which infected 500 million and killed 50 million worldwide).

There are initial signs that the virus, like other viruses in its family, including the common cold, is fading with the arrival of warmer weather. We have read comments from several prominent epidemiologists supporting this view.

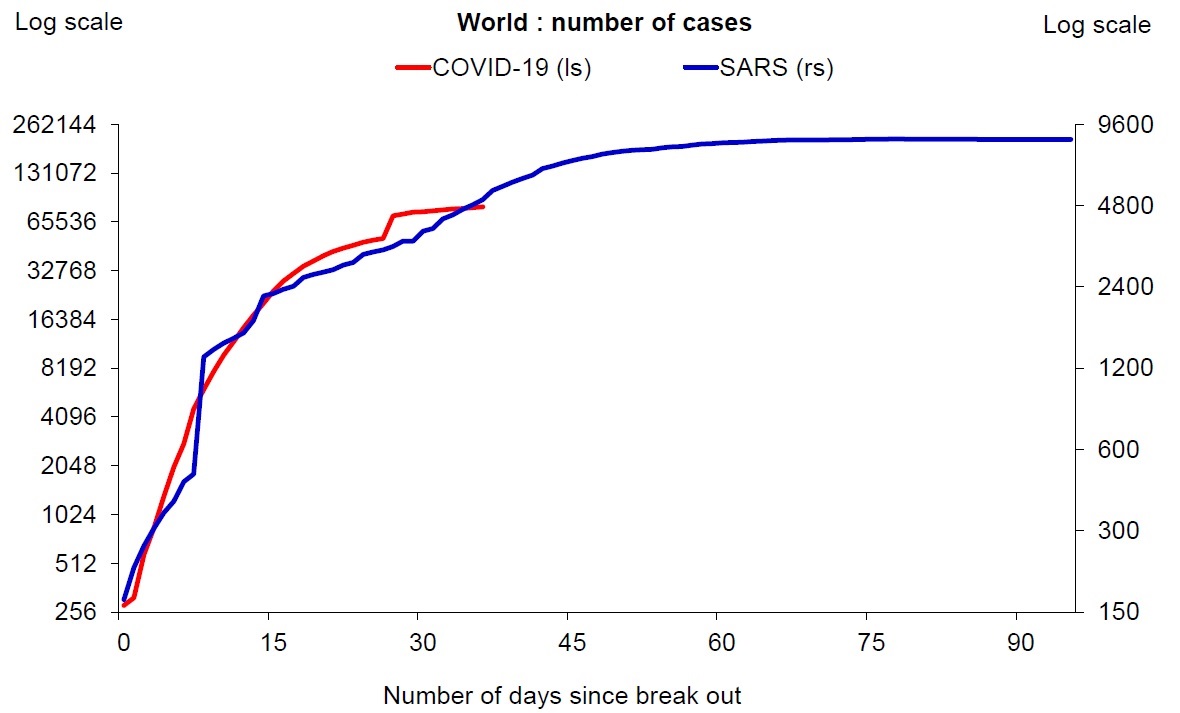

COVID-19 seems more transmissible than SARS, but much less deadly (SARS’ mortality rate was about 10%). It is following a similar trajectory and will likely plateau at a higher number of infections, but is approaching that plateau.

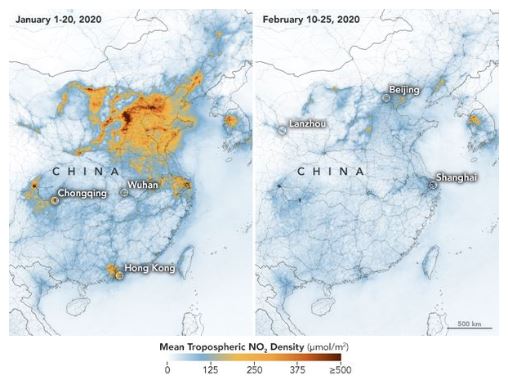

The virus-related slowdown in China will certainly extend into the second quarter, and February PMIs (purchasing managers’ indices) dropped to record lows. However, pollution and traffic data, as well as anecdotal data from manufacturers, suggest that China is now getting back to work. The government is widely anticipated to roll out very strong broad stimulus measures, to achieve the 5.6% GDP growth this year that would be needed to meet the longstanding goal of doubling the economy’s size between 2010 and 2020. (There will certainly also be more than the usual amount of statistical fudging.)

In summary, then, the data suggest (1) that COVID-19 will not be a devastating global “black swan” event, but will be the equivalent of a severe flu season; (2) that China will bear the brunt of the economic consequences, but (3) that it is already recovering, and (4) that the Chinese government will engage in a massive stimulus effort in an attempt to save face and meet its long-term growth target.

So What Really Happened Last Week?

All this presents a conundrum — if COVID-19 is not that bad, what happened last week? We believe that the unprecedented speed of last week’s decline reflected both widespread fear, and the 2007 demise of a Depression-era trading rule — the “Uptick Rule,” which for decades governed the behavior of short sellers.

Short sellers are speculators who profit from a decline in a security’s price. They accomplish this by borrowing the security with a promise to deliver it back at some future time. They then sell it immediately, hoping to be able to buy it back at a lower price before they need to return it. Of course, if at the end of the trade, the security has gone up in price, they will have a loss instead of a gain. Some people view short selling as pessimistic and opposed to the fundamental optimism that investors should have about the future. But short sellers can serve a valuable function, since they are strongly motivated to seek out unpleasant and uncomfortable truths about the companies they study. They can alert investors to problems that have been ignored or hidden, and they deserve to be rewarded for such useful activity.

However, short sellers can also exacerbate and accelerate stock declines that are unwarranted by a company’s fundamentals, since they create artificial selling pressure and can frighten long-term holders of a stock into selling, thus creating a self-reinforcing downward spiral in a stock’s price. The now-illegal process of “naked” shorting involves short-selling when the seller hasn’t borrowed the underlying shares — exploiting loopholes and disconnects between paper and electronic trading systems to effectively counterfeit shares and add to selling pressure.

In 1938, U.S. financial authorities instituted the “Uptick Rule,” which is intended to prevent this kind of cascade. It said that a short seller could only sell on an uptick, that is, if the last movement of a security’s price was up rather than down. For almost 70 years, that rule made it much more difficult for unscrupulous short-sellers to encourage and profit from a stock’s death spiral. But that rule was abolished in 2007, replaced by a rule that only activates the uptick restriction when a stock has already dropped 10% in a day.

We think that last week was an example of how, without the uptick rule as originally instituted, pessimistic or opportunistic short sellers can help create a self-fulfilling downward cascade. That was part of what made the decline so precipitous and unrelenting. We don’t know of any evidence that there was collusion involved, but we do note that contemporary algorithmic trading exponentially increases the ability of intelligent, high-tech short sellers to influence markets. The general panic about COVID-19 created the perfect environment for such activities to have a stronger-than-usual effect.

For our part, we believe that it would be in the best interest of all honest market participants for the original uptick rule to be reinstituted. We are happy to hear calls for this from several respected and eminent stock market observers and commentators. And this is not a matter of concern only to investors; it should concern everyone. The causal relationship between the markets and the economy runs both ways. It is not true simply that economic crashes cause market crashes. Market crashes can also help precipitate economic crashes, by destroying business and consumer confidence and alarming market participants by the evaporation of their wealth.

Investment implications: In an era when algorithmic trading comprises an ever-greater part of the trading volume of stocks, and there is no effective uptick rule in place to prevent short-selling pressure from contributing to irrational, self-reinforcing price declines, it is more important than ever for investors to base their decisions about when to buy and when to sell on the most dispassionately analyzed and neutrally reported data they can find. It is equally important to distinguish as sharply as possible between declines driven by fundamentals, and declines driven by algorithmic irrationality.

Related: The 6 Most Important Charts To Watch in Turbulent Markets

DISCLOSURE:The views and opinions expressed in this article are those of the contributor, and do not represent the views of Advisorpedia. Readers should not consider statements made by the contributor as formal recommendations and should consult their financial advisor before making any investment decisions. To read our full disclosure, please click here.