Written by: Joseph Burns | iCapital Network

Following a week when U.S. and global stocks rose by roughly 10%, including the “strongest 3-day percentage increase since 1931”1, investors are feeling a bit better about their equity portfolios. Still, even after that week of strong performance, equity markets are down (20%-30%) in 2020.

Much has been written about how this recent market decline, precipitated by the deadly COVID-19 pandemic, is not-at-all similar to the global financial crisis of 2008. While the primary causes behind the steep equity losses in both 2008 and 2020 are very different, the effect on the S&P 500 Index has actually been quite similar:

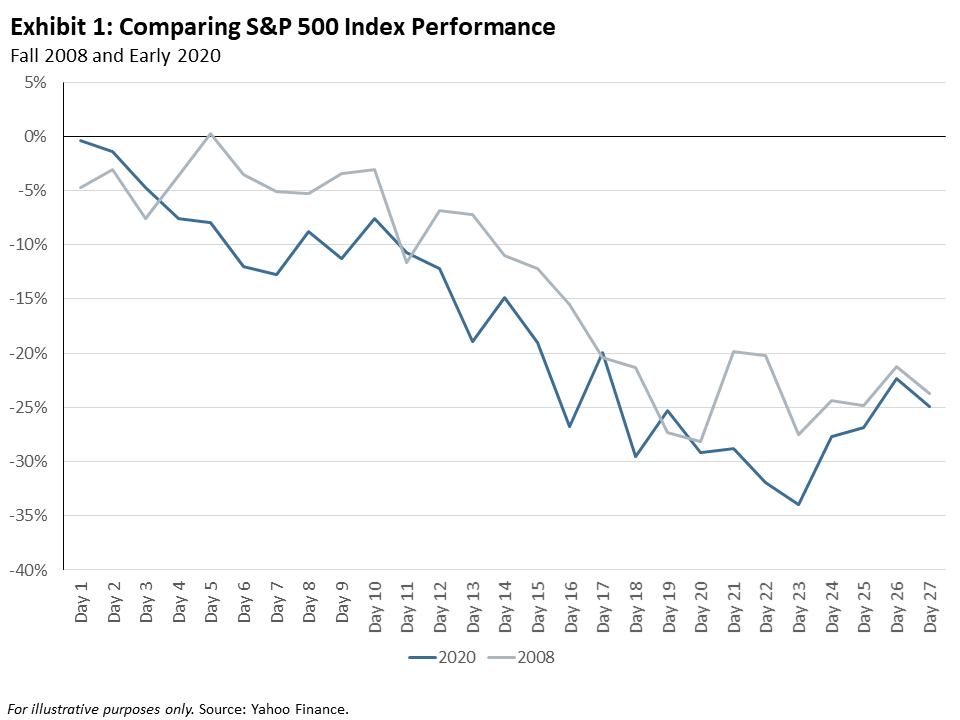

Exhibit 1 highlights the daily performance of the S&P 500 Index in the fall of 2008, just after the Lehman bankruptcy and the recent market performance since late February of this year2. The rally of late that continues as we head into month-end has been supported not only by the dramatic economic stimulus, but also by an investor mindset influenced by the prior 10+ years of market action. Since the Financial Crisis of 2008, each equity sell-off was typically met by an aggressively accommodative policy response, and any investor that pursued a “buy-the-dip” strategy was handsomely rewarded. It is not difficult to see why some investors have a high degree of conviction that, at least from a market perspective, the worst might be now behind us and the “temporarily disrupted” bull market in equities is already on the mend. A longer-term historical perspective doesn’t easily support that optimistic belief, however.

Sticking with the comparison the S&P 500 Index also rallied 10% over the course of a single week in October 20083. Back then, we saw many long-only equity managers pounding the table, enthusiastic about the buying opportunities. But, as is often the case during periods of severe market dislocations, the downward pressure on equities persisted for several months following the initial market sell-off.

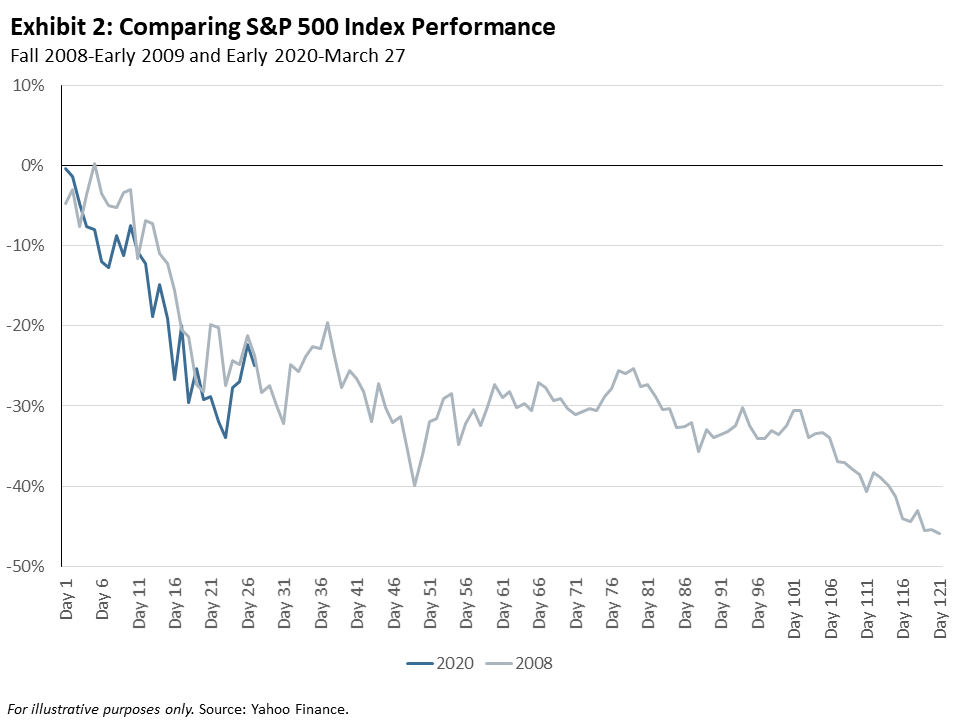

Exhibit 2 extends the time period into early 2009. That market decline lasted another 4-plus months. In fact, following the earlier 10%-plus snapback rally, the Index proceeded to fall by another -30%, bringing the total drawdown to nearly -50%. Clearly, the most aggressive investors in the early days of the 2008 market sell-off suffered a “double whammy” of (a) initially losing -30%, recouping some losses, perhaps feeling emboldened or fearful of missing out, and then (b) seeing the value of their long-only equity investments depreciate by a similar order of magnitude over the subsequent months. Back then, it took a full 2+ years for markets to return to their Sept. 2008 levels4.

So, what can Advisors do to drive performance and maintain exposure to appreciating assets, without subjecting clients to significant downside risk? Back in 2008, as in the current environment, the risk-reward characteristics of other financial assets and strategies less sensitive to directional equities provided opportunities for substantial portfolio gains. Examples include actively managed funds focused on securities higher in the corporate capital structure, many of which have been sold off considerably and are likely to go through complex events to unlock future value. The current market is estimated to have over $1 trillion of securities now trading at distressed levels5. These include both investment grade and high yield bonds, leveraged loans, municipals, structured credits and opportunistic equities. In many cases, their future price is linked directly to company-specific fundamental values, pending corporate events and identifiable near-term catalysts, and these securities are far less dependent on equity indices returning to their previous highs.

Many market prognosticators and industry leaders are once again suggesting that now is the time to get back into the stock market. That certainly may prove to be a prescient call. If nothing else, the majority of publicly traded stocks are “on sale” compared to their market prices from just one month ago. Investors must tread carefully, however, given the uncertainty around the long-term COVID-19 effects on the global economy, combined with the risk of weaker-than-expected earnings, declining revenues, slowing growth, falling profit margins, and the potential for a substantial increase in defaults and corporate bankruptcies. Ultimately, a well-constructed and broadly diversified portfolio will provide the most significant long-term value, and the best risk-reward opportunities in the current market may not be realized in publicly traded, long-only equities.

While the market risk obviously pales in comparison to the human toll associated with this global pandemic, properly considering the past is usually a pretty smart way to prepare for the future. Case-in-point: that earlier reference to the “strongest 3-day percentage increase since 1931” should be put into its proper context. That 1931 rally occurred in the midst of a peak-to-trough equity decline of 86%, with the market taking a full 22-years to reach new highs. We can all hope that history doesn’t repeat itself.

We are clearly living in a world filled with tremendous uncertainties, and for those of us who interact with clients, the responsibility we share in providing thoughtful guidance and actionable recommendations never stops. Sound advice is most valuable whenever uncertainty peaks. From our perspective, the most attractive investments on a risk-adjusted basis today reside in a few specific areas: catalyst-driven equities, and specialized credit investing across public, structured and private market strategies, including, of course, experienced stressed and distressed investment managers. Passively managed, daily-liquid vehicles that invest in these types of assets have potential liquidity risk, while long-only public equities have the potential to elevate downside risk in client portfolios. Delivering returns with an acceptable level of risk is the primary job of any Investment Advisor, and sourcing the best risk/return opportunities is an essential component in helping clients achieve their long-term goals.

In addition to the more important things in life brought on by the current crisis – like spending more time with loved ones, reading a few classic novels, or trying to learn a new language or an instrument – binge watching new (or old) TV shows has become a popular pastime. I admit to having recently watched back-to-back episodes of an old, personal ‘80s favorite, Hill Street Blues. As some may recall, the concluding comment from Sergeant Esterhaus after every meeting was the same, and it serves as a great bit of advice regarding our collective experience in this strange new world, and can easily be used in the context of investing in the current environment. Let’s all be careful out there.

Related: Does Gold Really Care Whether Coronavirus Brings Us Deflation or Inflation?

1) Nasdaq, "Dow Wraps Up Strongest Three Days Since 1931," March 26, 2020.

2) Specifically, for the periods: (a) Sep. 15th through Oct. 21st, 2008, and (ii) Feb. 20th through Mar. 27th, 2020.

3) The S&P 500 Index rose by 10.5% from Mon. Oct. 27th through Fri. Oct. 31st, 2008, excluding dividends.

4) Extending this look-back period to Oct. 2007 - it took 5½-years for the S&P 500 to recoup its losses (in Apr. 2013).

5) Generally defined as securities trading with at least a 10% yield over U.S. Treasury bonds.

DISCLOSURE:The views and opinions expressed in this article are those of the contributor, and do not represent the views of Advisorpedia. Readers should not consider statements made by the contributor as formal recommendations and should consult their financial advisor before making any investment decisions. To read our full disclosure, please click here.