In mid-to-late 1998, Ralph Acampora, CMT the head technical analyst at Prudential, began getting bearish on the stock market as he grew concerned about the narrowing breadth landscape for U.S. equities. In Bull! by Maggie Mahar, Acampora is to have said “they’re shooting the generals.” One of the founders of the Chartered Market Technician designation, Ralph’s realization at the time of the importance in evaluating the market’s leadership as a clue into the health of the bullish trend was poignant and marked one of the early developments in the last gasps of the dot-com bubble.

Top Five

To extend Ralph’s notion of “Generals” to today’s market I think we could look at it from two angles. First, the largest stocks in the S&P 500, which now account for over 20% of the index – the largest percentage since 1978 according to Jim Bianco. We’re now at a point that exceeds the few “generals”’ of the 2000s (when the top five peaked at 16.6%), giving even more reason to focus on these mega cap stocks that cause the waves ridden by the entire index. A few years after the prior high in the late-70s, oil-related securities were at the top of the S&P, representing almost a fifth of the indexes value. And then in 1980, oil dropped and brought down the oil generals and with it the S&P 500 by 27%. When the generals are no longer left standing, its hard for the remaining solders to hold their ground.

In fact, Goldman Sachs recently noted that through the end of April of this year, the top five have produced a 10% gain while the remaining companies are still down 13%. If we get an idea of what these five are doing, then we should have a better sense of the health – or lack thereof – for the S&P 500 as a whole. History has shown us the importance of the “generals” and so we don’t want to lose track of their price action.

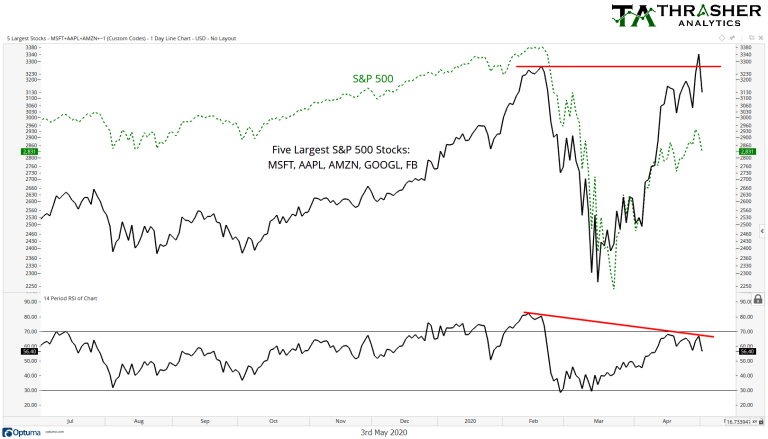

The chart below shows a composite index of the five: Microsoft, Apple, Amazon, Alphabet (Google), and Facebook. These five were leaders at the low in March, bottoming on March 16th ahead of the S&P 500 low on March 23rd. From there they rallied back above their collective February high but here recently experienced some trouble. As of last week, the composite index has fallen back below the February peak and with it, a lower high in momentum based on the 14-day Relative Strength Index (RSI).

Positive Performers

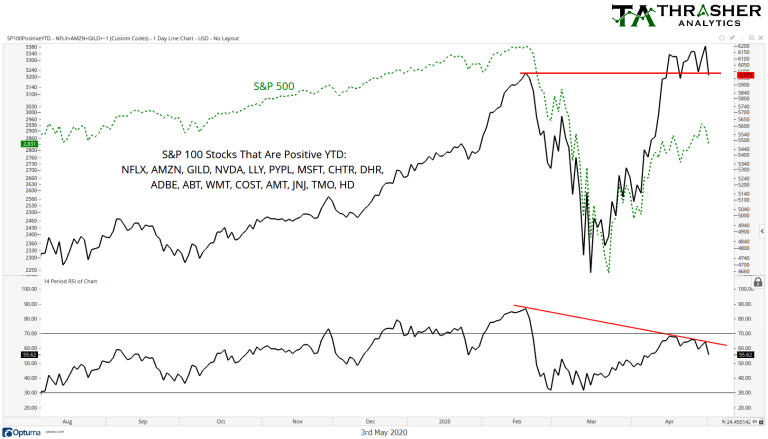

Another way we can evaluate who the “Generals” are can be based on performance. Sticking with our focus on larger cap companies, I built another composite index of the only stocks within the S&P 100 that have positive year-to-date performance through Friday (May 1st). Unfortunately, this list is fairly short with just seventeen names – many of which are also included in the prior list of the five mega caps.

Once again, we have this group of market leaders bottoming ahead of the index, showing their leadership status as they marched back above the February high. However, momentum has been declining since mid-April, making lower highs each time the composite eked out a slightly higher-high. By the end of last week this group of positive YTD performers were inching back under the February high as they begin to confirm the bearish divergence observed in momentum.

Do these potential false breakouts (above the February highs) signal the countertrend in equities has ended? We will likely soon find out. If we aren’t seeing strength in the five largest stocks and we aren’t seeing bullish price action in the names that have at least pulled out a gain in the first four months of the year, then we’ll need to see some major rotation…and quick.

As Ralph appropriately cited back before the dot-com peak, the “generals” of today’s market appear to be taking on fire. If they go un-defended, then we could see the broad market also weaken as it did in 1980 and begin a path back near the merciless March low.

Related: Why Volatility Suggests Further Equity Weakness May be In Store