When the unexpected happens

There are always some who question the value of insurance – money that leaves the spender feeling as though it might be deployed elsewhere with better returns and no ill consequences. But then the unexpected happens – a flood, a fire, a burst pipe, an illness – and that insurance quickly looks like a very prudent move.

We occasionally hear similar arguments about the use of liquid alternatives in an investment portfolio. Most often, it arises during periods when the economy is growing and the stock market is on a steady uphill climb, much like we’ve experienced for most of the last decade. But then stocks experience something like a 30-year flood – the mortgage crisis, the .com crash – and you’re reminded again of life’s unpredictability.

Since the start of the year, we seem to keep writing about these ‘exogenous” events, a kind of bloodless term that doesn’t really capture the human cost of the kind of situation we’re now experiencing as the world grapples with the novel coronavirus. Six months ago, the idea that such a virus would emerge in China and quickly spread to dozens of countries was not high on the list of worries for most market participants. Today, it’s all anyone is talking about.

Worries over this outbreak triggered a four-day, -11.44% plunge in the S&P 500 in the last week of February – the fastest market correction on record – and included the largest one-day points drop in the history of the Dow Jones, a fall of nearly 1,200 points. As an investor, when things are smooth in the markets, it’s easy to tell oneself that you’ll be able to ride out sudden volatility without making a rash investment decision. Maybe you’ll even be one of those select few who can be “greedy when others are fearful,” to quote the Oracle of Omaha. But in reality, it’s very hard to remove emotion from the equation when faced with what feels like a plunging market.

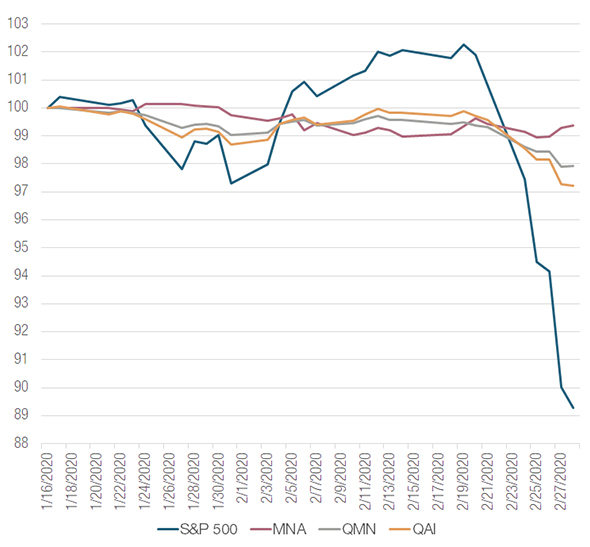

The only real defense is to be prepared, and to stay diversified. Our three liquid alternative exchange-traded funds (ETFs) – the IQ Hedge Multi-Strategy Tracker (QAI), IQ Merger Arbitrage ETF (MNA), and the IQ Hedge Market Neutral Tracker (QMN) – have all shown considerably less volatility and lower drawdown than the broad market during this latest sell-off through February 28, 2020. That is consistent with the intent of the underlying strategy, and with the historical performance of these funds since inception.

Source: NYLIM 3/4/2020 Past performance is not indicative of future results. An investment cannot be made in an index. The S&P 500 is a stock market index that tracks the stocks of 500 large-cap U.S. companies. It represents the stock market’s performance by reporting the risks and returns of the biggest companies.

Investors are confronted with two major decisions in times like these. First, does it make sense to reduce market exposure? Second, if you do sell into this decline, when do you get back in?

To fully benefit from a drawdown, you have to get your answers to both of these questions more or less right, an almost impossible task.

That’s why it’s good to stay diversified and to keep in mind that, over time, economies recover, and equity markets have been inclined to go up. Not every day or every week – and some days and weeks are definitely worse than others – but over the medium- and longer-term.

Flood insurance doesn’t seem that valuable when the sun is out (except, maybe to provide some peace of mind). But the sun doesn’t always shine. Similarly, markets don’t always go up. Well-constructed liquid alts strategies can play a major role in both times of calm and times of turbulence.

The potential for generating positive returns will be there when markets are flat or trending up (meaning the cost to carry your “insurance” may be lessened, should we stretch the insurance metaphor one step further) while they can also help investors manage volatility when the unexpected inevitably comes along.

Related: The Dollar Zigs When It Was Predicted to Zag

DISCLOSURE:The views and opinions expressed in this article are those of the contributor, and do not represent the views of Advisorpedia. Readers should not consider statements made by the contributor as formal recommendations and should consult their financial advisor before making any investment decisions. To read our full disclosure, please click here.