This week's mixed messages on labor conditions and inflation are confounding market participants and causing bifurcated action across equities and fixed income. Stocks lost ground in early morning trading alongside bonds, but weaker-than-expected ISM services figures served as an interception, turning the ball over to equity bulls. Bond yields are still climbing, however, in response to a much stronger-than-anticipated ADP Jobs report and cooler but still elevated euro inflation numbers.

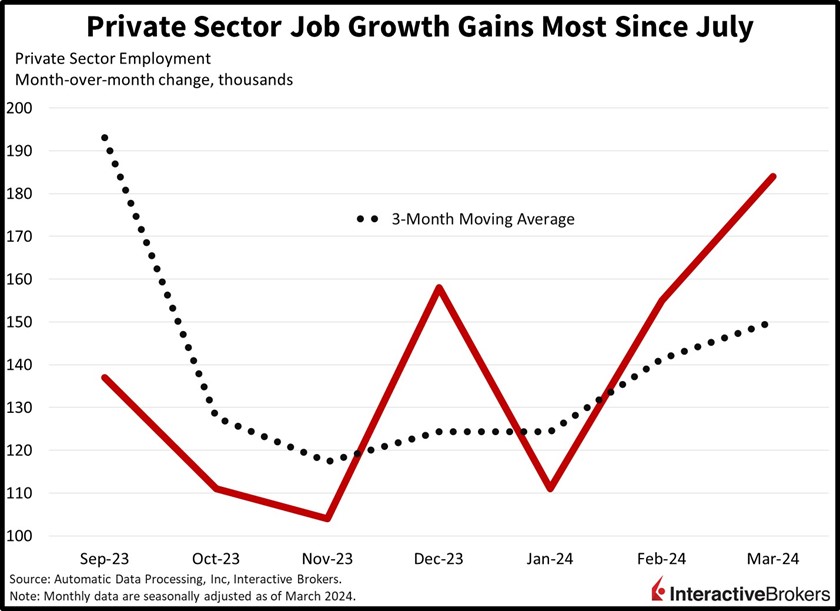

ADP Data Depicts Strong Hiring

Employers accelerated their rate of snatching up workers in March and continued to increase the size of paychecks, underscoring that labor market conditions remain robust. Private payrolls jumped by 184,000 last month, up from the revised 155,000 additions in February, according to this morning’s ADP data release. In addition to climbing significantly month over month (m/m), job additions exceeded the analyst consensus expectation of 148,000. It was the strongest month for job gains since July and hiring was positive in all sectors except for the professional and business services category, which lost 8,000 positions. The leisure and hospitality sector led the hiring splurge with 63,000 new positions followed by construction, which added 33,000. Other sectors with expanding headcounts and the number of jobs added include the following:

- Trade, transportation and utilities, 29,000

- Financial services, 17,000

- Education and health services, 17,000

- Other services, 16,000

- Natural resources and mining, 8,000

- Information, 8,000

- Manufacturing, 1,000

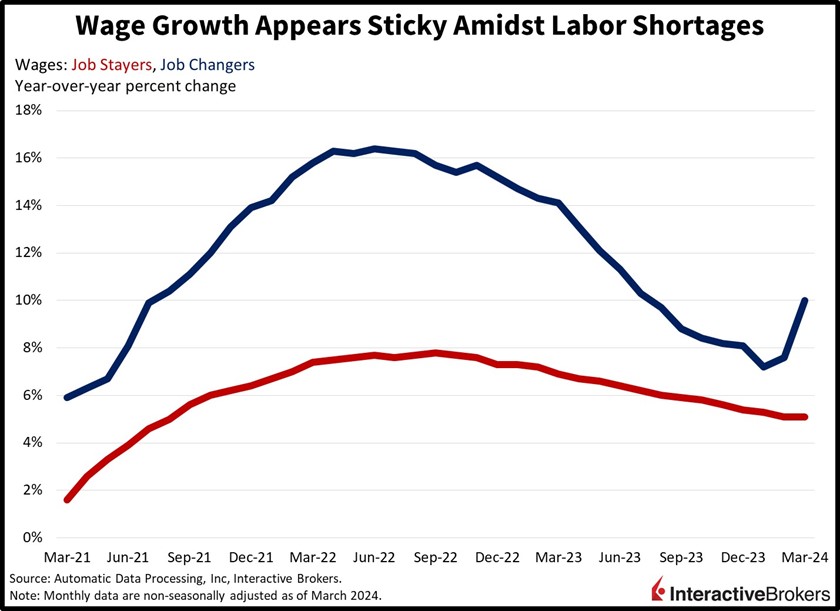

Mid-sized companies (50-499 employees) led the hiring effort by adding 93,000 workers. Large (500+ employees) and small companies (1-49 employees) brought on an additional 87,000 and 16,000 employees, respectively. From a regional perspective, the South added 91,000 jobs while the West and Midwest added 53,000 and 28,000 positions. The Northeast added 20,000. Strong labor demand was also depicted by compensation, with job changers securing 10% pay increases year over year (y/y), a sharp jump from February’s 7.6%. Other employees experienced a 5.1% median pay increase, meanwhile, unchanged from the previous month.

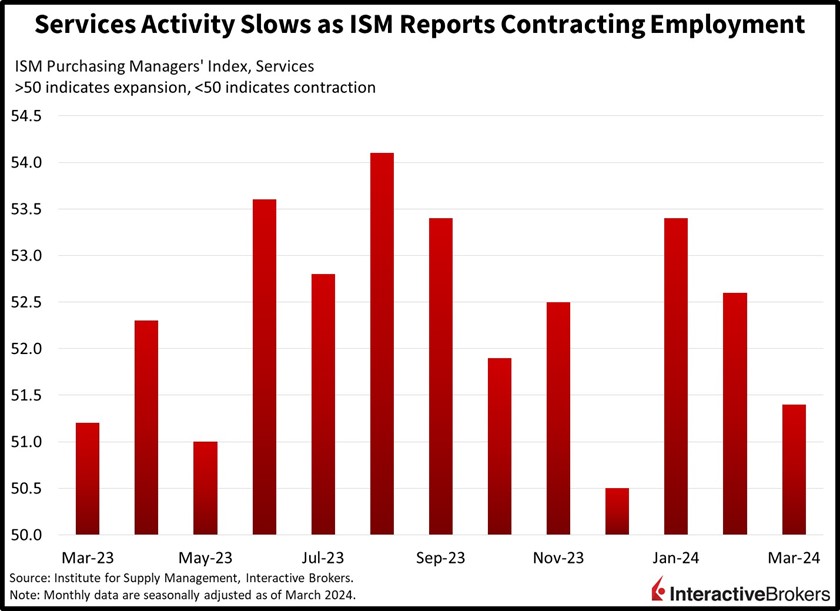

ISM Data Depicts a Different Story

ISM Services data threw a curveball shortly after the ADP release, with the report delivering a headline miss alongside a contraction in employment. The overall March figure of 51.4 declined from 52.6 during the previous month and missed the estimate of 52.7. A sizable contributor to the miss was a reduction in headcounts, with firms reporting challenges associated with labor costs and trouble with replacing former employees. Employment registered a rate of 48.5, better than February’s 48 but still below the expansion-contraction threshold of 50. Production, new orders and prices offset the hiring weakness, coming in at 57.4, 54.4 and 53.4. New orders and prices slowed from the previous month’s 56.1 and 58.6, which served to propel the equity market turnaround.

Eurozone Inflation Eases, But Is Still Elevated

Prices rose sharply in the eurozone last month with goods costs driving the increase. Inflation gained 0.9% m/m but only 2.4% y/y, compared to February’s 0.6% and 2.6% and near expectations. Similarly, core inflation, which excludes food and energy, rose 1.1% m/m and 2.9% y/y. The figures reflect a dynamic of short-term acceleration while the longer-term readings cooperate with efforts to tame inflation. Goods and services drove the monthly incline, with prices rising 1.9% and 0.7% m/m. Also pushing up costs was the processed food, tobacco and alcohol category, with prices rising 0.3% m/m. Unprocessed food and energy offset some of the overall pain with charges declining 0.6% and 0.3% during the period.

Stocks Run with Interception

Stocks have recovered from earlier losses following the ISM-Services release, but bonds are still selling off. All major US equity indices are higher, led by the 0.7% gain of the Russell 2000 Index. The Nasdaq Composite, S&P 500 and the Dow Jones Industrial indices have climbed 0.5%, 0.4% and 0.3%. Sectoral breadth is positive with 8 out of 11 categories higher, led by industrials, technology and energy, which have produced gains of 0.7%, 0.7% and 0.6%. Consumer staples, real estate and utilities are the only decliners, losing 0.7%, 0.2% and 0.1%. Yields are marching higher as bond investors focus on hawkish comments from Atlanta Fed President Bostic, who recently reiterated his belief that only one rate cut will occur this year in the fourth quarter. Rates watchers also prioritized rising oil prices, firm ADP jobs data, and strong Euro inflation numbers rather than weaker ISM-Services readings. The 2 and 10-year Treasury maturities are trading at 4.72% and 4.39%, 3 and 4 basis points (bps) higher today. Loftier yields aren’t helping the dollar though, with the currency’s index down 38 bps to 104.35, as the greenback loses ground relative to most of its major developed market counterparts, including the euro, pound sterling, franc, yuan and Aussie and Canadian dollars. The US dollar is up versus the yen though. Oil is continuing its bullish trend and is being supported today by OPEC+ ministers maintaining their output restriction commitments and geopolitical concerns in the Middle East and Far East possibly leading to supply disruptions. Supply conditions stateside are also helping, with the Energy Information Administration reporting surprise draws across most of the industry today. Oil bulls aren’t currently worrying much that the White House is suspending its Strategic Petroleum Reserve refill since prices have risen so much. WTI crude is up 0.6%, or $0.50 to $85.89 per barrel.

Making Sense of Conflicting Data

Today’s crosscurrents may be reconciled in the short term with this Friday’s Jobs Report containing the most significant data points so far this month. The totality of the recent data, however, points to an economy that’s growing strongly alongside rising prices. Over in Europe, though, economic performance is near the flatline even as costs increase, warranting a situation where the ECB cuts before the Fed, due to recession risks. Here in the states, however, economic activity is buoyant amidst consistent hiring, but global investors believe that both central banks will begin their respective easing cycles in unison, perhaps this June, even as conditions in both regions are starkly different. At the moment, though, high and rising oil prices are the greatest threat to monetary policy easing prospects.

Related: Manufacturing Recovery Met With Fiery Price Pressures