Hot manufacturing data stateside and across the Pacific in Beijing is sending yields higher and stocks lower. Market participants are concerned that the goods sector’s return to expansion may bring back a familiar foe. Indeed, the global manufacturing recession was a protagonist for disinflation last year, but progress is now reversing, with inflation accelerating strongly. Against this backdrop, the Fed’s first rate cut may arrive in the second half of the year after all, with probabilities of a reduction this June inching closer to coin-flip odds.

US Manufacturers Report Price Increases

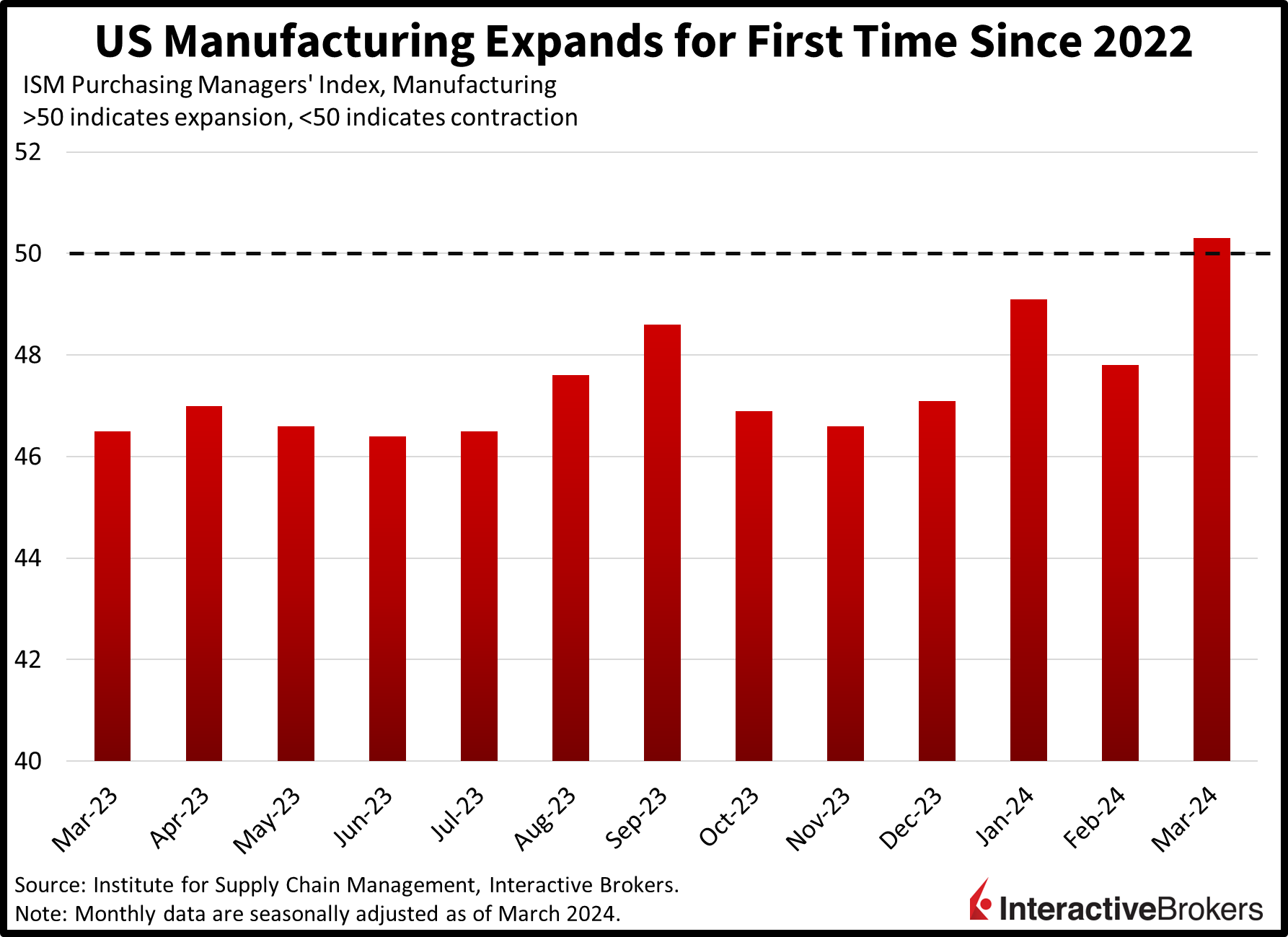

Manufacturing activity in March expanded for the first time in 17 months as reported by ISM’s Purchasing Managers’ Index (PMI). Last month’s 50.3 reading battered projections of 48.4 and grew strongly from February’s 47.8. Unfortunately, though, the greatest segment driving the upside surprise was prices, which came in at a lofty reading of 55.8, accelerating from the previous month’s 52.5. Also helping the headline figure were production, imports, exports, and new orders, which scored 54.6, 53, 51.4, and 51.6. Manufacturers are indeed doing more with smaller headcounts as employment contracted, sporting a figure of 47.4. Inventories contracted while delivery times quickened on a month-over-month basis (m/m).

US Construction Weakens

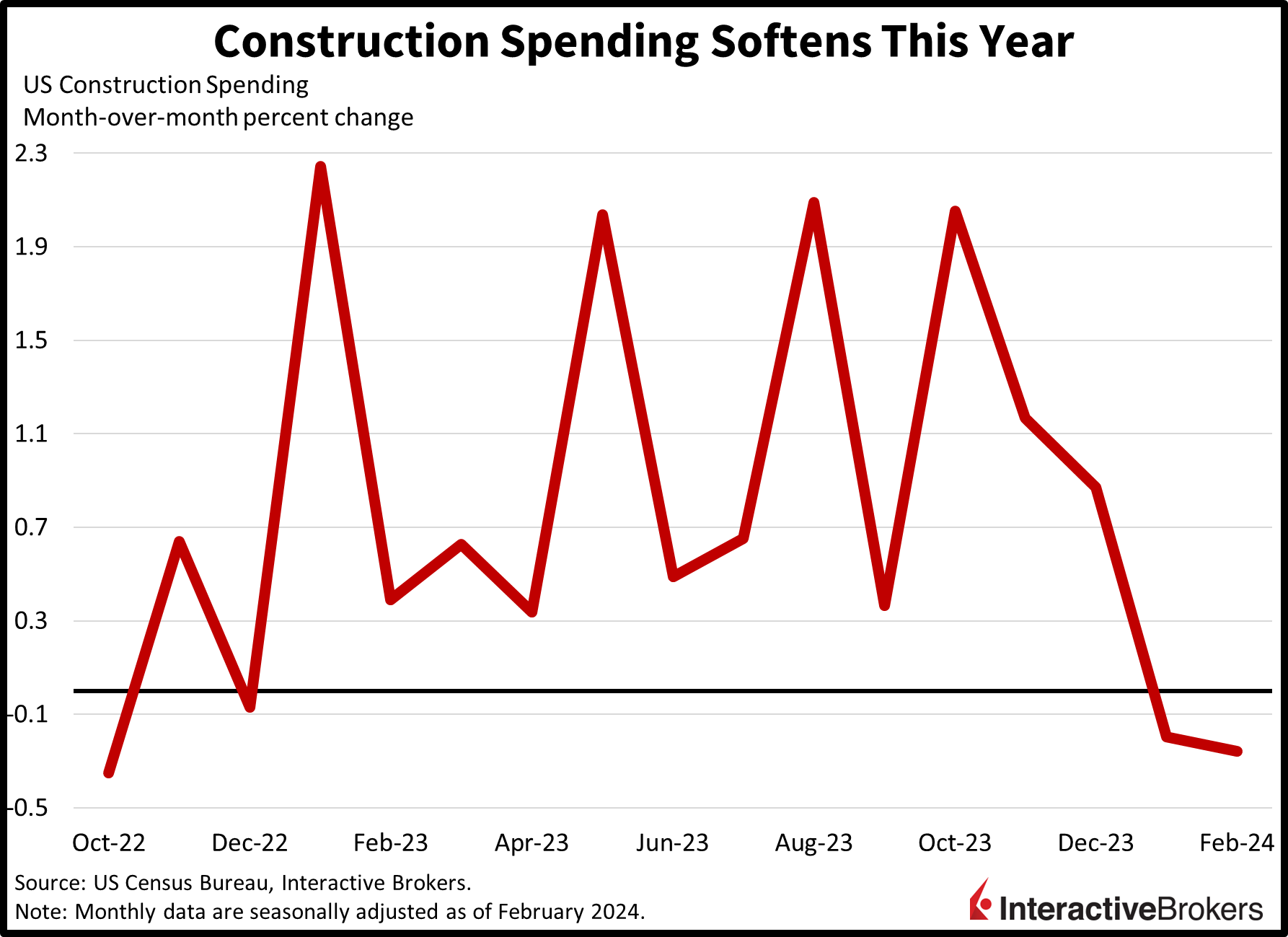

Construction spending contracted in February even as building activity for residential real estate strengthened. Total construction spending decreased 0.3% m/m, much worse than the 0.7% growth anticipated and a steeper rate of decline relative to January’s 0.2% contraction, according to this morning’s Commerce Department data release. Residential investments grew 0.7% m/m, with new single-family homes increasing 1.4%, while new multifamily investments dropped 0.2% during the period. The transportation segment also helped, growing 0.7% during the period. Among the 16 non-residential categories, 15 of them sported declines, with health care, commercial, and water supply weighing on results by dropping 2.2%, 1.9%, and 1.8%. The highway and street, amusement and recreation, religious and educational areas all fell 1.5% m/m.

China Stokes Optimism of Economic Recovery

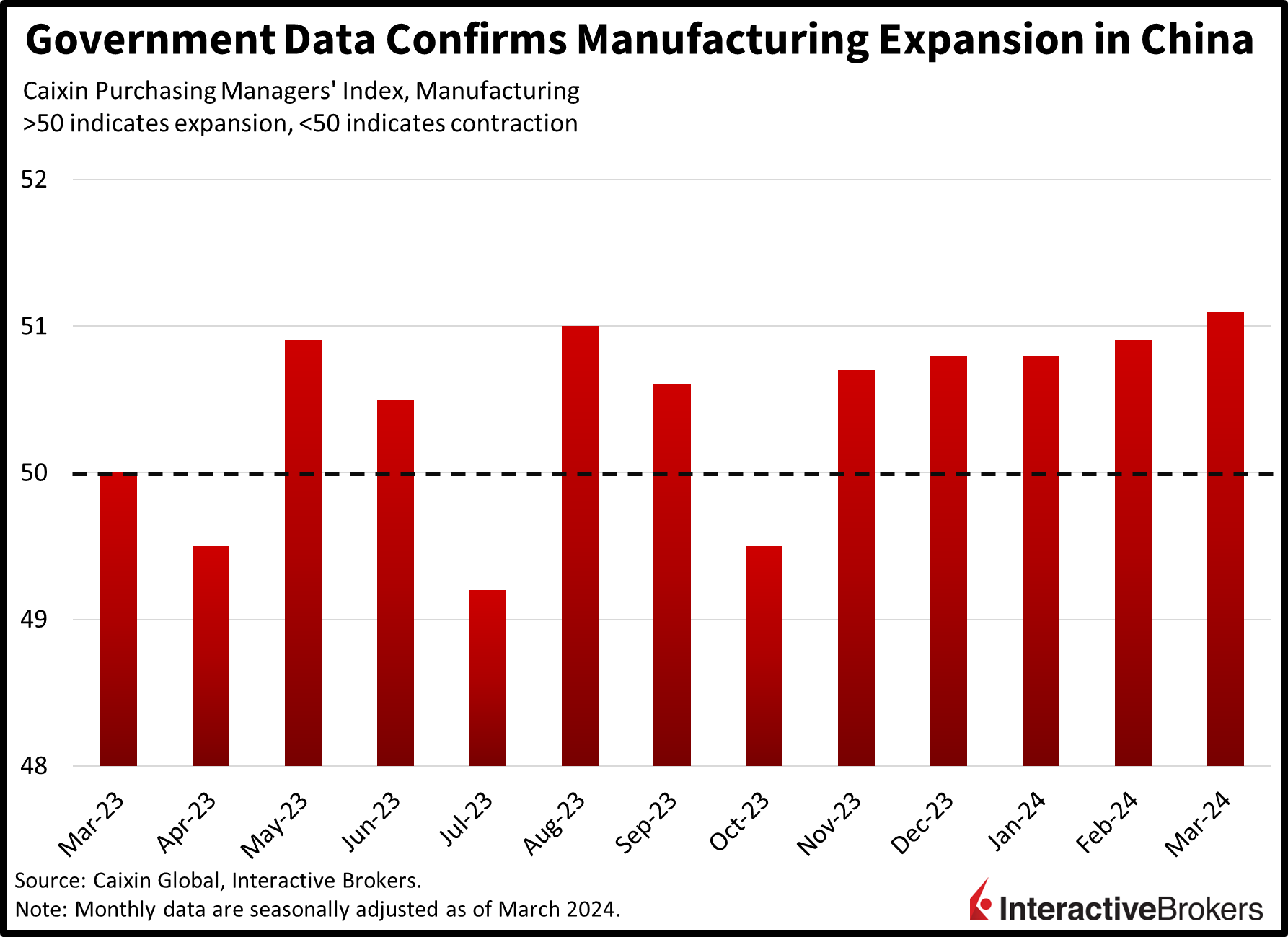

Beijing also dished out stronger-than-expected manufacturing data, sparking optimism that the country’s limping economy may be improving. After five months of decline, the government’s manufacturing PMI exceeded the expansion/contraction threshold of 50 with a March result of 50.8. It climbed from 49.1 in February and beat the median analyst forecast of 50.1. The benchmark’s new export order category climbed to 51.3, the first time in a year that it has expanded. The export order gauge points to a likely increase in March exports, which would be the third consecutive month of gains. On a broader level, overall orders reached 53, a 12-month high. Separately, the Caixin manufacturing PMI hit 51.1, its fifth month above the expansion/contraction threshold. Analysts anticipated a score of 51.0. China also said non-manufacturing employment contracted to the lowest level in five months as travel volume weakened after the end of the Chinese New Year.

Markets Wobble on Fed Fears

Markets are selling off with all major US equity indices lower as bond yields, the dollar and oil prices soar. Investors are indeed front running the possibility of yet another hawkish pivot from the Fed. While the odds of Powell turning increasingly hawkish are low, taking profits in April seems prudent considering that stocks are already up 11% year to date. The year has just started, ladies and gentlemen. The Dow Jones Industrial, Russell 2000, S&P 500 and Nasdaq Composite indices are lower by 0.7%, 0.7%, 0.3% and 0.1%. Sectoral breadth is deeply negative with 10 out of 13 sectors lower, led by real estate, healthcare, and utilities; they’re down 1.2%, 1.1%, and 1%. Energy, communication services, and technology are higher by 0.5%, 0.3%, and 0.1%. Rates are soaring as the manufacturing comeback amidst loftier oil prices boosts inflation expectations, which are also delaying projections for the Fed’s first rate reduction. The 2- and 10-year Treasury maturities are trading at 4.72% and 4.32%, 9 and 11 basis points (bps) higher on the session. The possibility of a firmer Fed and loftier yields are supporting the US currency, with the Dollar Index up 46 bps to 105. The greenback is up versus all major, developed market counterparts except for the yuan, which is benefiting from upbeat manufacturing data in the export-dependent nation. The US dollar is gaining relative to the euro, pound sterling, franc, yen, and Aussie and Canadian dollars. Crude oil is surging on bullish supply-demand dynamics. Namely, the supply side is being constrained by OPEC+ concerns and continued attacks from Kyiv upon Russian refineries. The demand angle is being buoyed by better data out of Beijing, the world’s largest oil importer. WTI is trading higher by 1.4%, or $1.14, to $84.20 per barrel.

The Fed Gives Up on 2%

While stock investors are concerned today about delayed interest rate reductions from the Fed, it’s important to remember that monetary policy is much more than just the rate itself. Think about how long we’ve been in a so-called “restrictive landscape,” but when you leave the circus and enter reality, financial conditions are much looser than they were before the Fed’s first rate cut in March 2022, pointing to an abundance of liquidity, animal spirits, and inflationary pressures. When you consider funds in the reverse repo facility, the size of the Fed’s balance sheet, the dovish commentary from Powell, nose-bleed fiscal spending, corporates flush with cash, and homeowners sitting on 2% mortgages, the economic environment is quite buoyant. That’s especially true when you remove the uncertainty of more rate hikes. Powell is terrified of another repo crisis that would be similar to the one that occurred when they were cutting the balance sheet pre-pandemic. But he didn’t seem concerned at all when they were adding $120 billion a month in 2022, even as inflation was raging. This Fed has implicitly accepted inflation at 3% to 3.5%, will not allow a traditional business cycle to play out, and is already planning ahead of the bond vigilantes by changing rules in the banking system. Its goal is that financial institutions can absorb much more Treasury issuance. While valuations are expensive, the one-two punch of accommodative fiscal and monetary policies are supportive of risk assets.

This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related: New Home Sales Slip as Investors Reexamine Rate Cuts