According to the CME Group’s FedWatch Tool, the market is expecting a 2 to 3 interest rate drops of 25bp each.

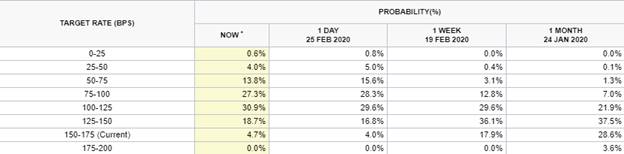

The following graph from CME shows the probability of what the December 16th meeting Fed Funds rate would be as compared to 1 week and 1 month ago.

In the post Financial Crisis era, the market is conditioned to believe that, each time investors feel uncomfortable, the FOMC will come to the rescue and take “necessary” monetary policy action. One can make the case that the market (thinly disguised as financial condition) is the tail that wags the FOMC dog. In fact, last year’s mid-cycle adjustment of 75bp is a great example of how the stock market was uneasy about the U.S.-China trade war and felt that the interest normalization process went too far; Chair Powell pivoted and capitulated.

It is public knowledge and obvious that, at the current 150-175bp rate, the FOMC has insufficient room (by historical standards) to stimulate the economy when the next economic recession or significant slowdown comes. However, the market is only focused on the present rather than the future. The market is suffering from a cognitive bias known as hyperbolic discounting, where investors choose smaller, immediate rewards rather than larger, later rewards, resulting from the fear of loss in the equity market.

Since the Great Recession, the FOMC has dropped rates when it sees or anticipates a case of financial tightening. The idea being that, when the rates are lowered, it would encourage investments (capital expenditure) and make the cost of borrowing lower to stimulate consumer expenditures. A side benefit is making the U.S. dollar more competitive, and that helps the exporters.

The question is would lowering rates by the FOMC now generate the desired outcome of safeguarding a slowdown in economic activities. I suspect not. The current market correction is certainly a fear-based response to a pathogen that kills 3 out of every 100 infected lives. For many investors who have made double digit returns last year, they rather take their chips of the table and contributed to the current downward spiral.

The supply (the supply and value chain disruption through work stoppage, closing of borders, ports and transportation stoppage, quarantining of cities and regions, and closures of factories) and demand (consumers homebound; malls, shops, entertainment venues, and restaurants closed; salaries and wages threatened; overseas travel and shopping trips deferred; conferences canceled; and liquidity for businesses and individuals running low) shocks that started in China are rippling through the rest of the world. The question is when the peak will come and if the impacts on the local and global economy are temporary or if the destruction is more permanent.

If you are scared of coming in contact with someone who may have contracted the Coronavirus, or if you are in a state of heightened alert, lower borrowing cost would not change your instinct to stay put and to go spend like a drunken sailor. FOMC lowering rates is ineffective towards warding off the transmission of the virus or changing the auto-behavioral response to hold back in the face of fear and uncertainty.

Last year, it was clear that, after two years of the China/U.S. trade war, most companies have held back on their capex and U.S. and European consumers have been holding the world economy together. Now, with pervasive fear and uncertainty, investors should be wondering if the demand shock is temporary or more long lasting which would pull the last leg out of world economic growth. However, if the policymakers following the old playbook of lowering rates and expect to stimulate the economy, the intended effect would not be there until confidence is restored regarding virus containment. The longer this goes on, the more likely aggregate demand will take longer to be restored.

We are seeing the limits of monetary policy, and we advocate for the FOMC to stay the course and don’t waste any more interest rate bullets.

Related: How Will Asset Managers Find Ways to Distribute Going Forward?