Written By: David Nelson, CFA CMT

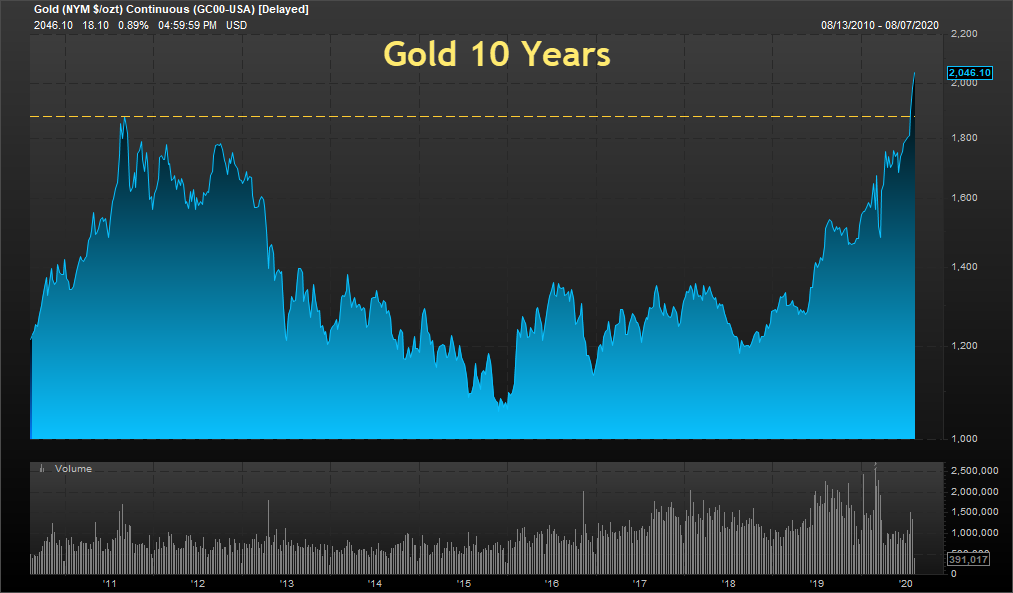

One look at any trader's stock monitor, and the numbers scream the obvious. Both risk-on and risk-off investments are working side by side in a market that has surprised both retail and institutional investors. On the heels of a pandemic and a market that fell 35% in just 23 trading days, gold, the ultimate safe haven, broke through an all-time high last seen in September 2011 and hasn't looked back.

Shed no tears for stocks because the S&P 500 is up over 53% from the March 23rd low and is less than 2% from another all-time high — something the Nasdaq 100 achieved all the way back in June. Unfortunately, the market cap tilt toward large cap secular growth in both the S&P and Nasdaq gives a less than perfect picture on the true health of the economy. While it picks up the economic windfall for companies like Netflix and Amazon, it masks much of the economic pain in your local community. The market is a fabulous tool and strong leading indicator for economic activity, but you have to be looking at the right market. More on that later.

In hindsight the case for gold was obvious given the Federal Reserve's race to zero forcing down the short end of the curve, leaving investors with few safe haven choices. The argument against gold as a non-income producing investment means little when the alternative is parking money for 10 years to earn a miserable 55 basis points in a U.S. Treasury. The first gold coins appeared in 700 B.C. and, of course, have a history as a store of value long before that.

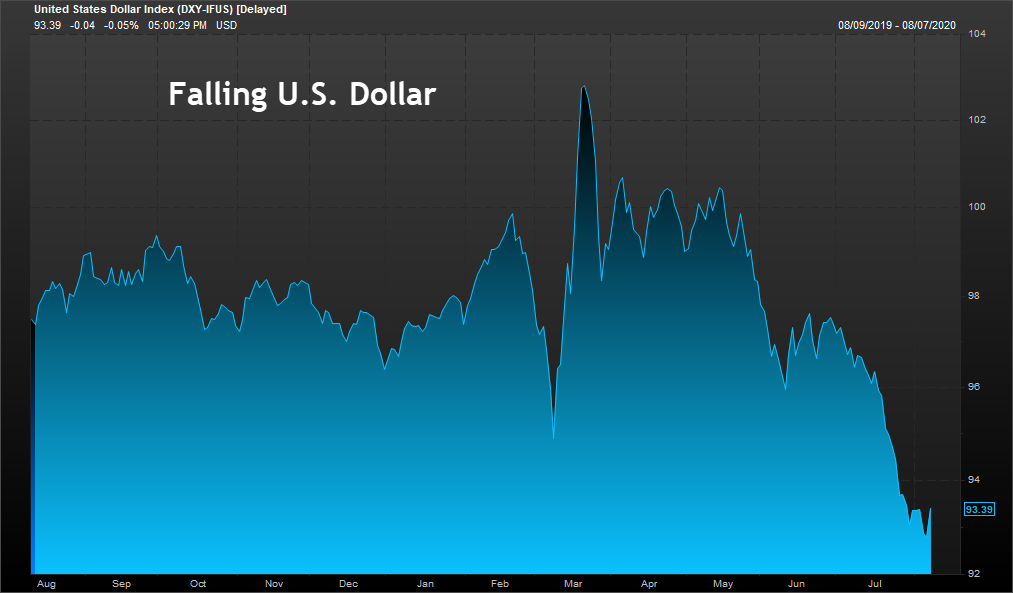

Gold and other precious metals get the added boost from negative real rates (nominal interest rates minus inflation) not to mention the add-on effect of a cratering dollar boosting the value of any hard asset.

Interestingly, the falling dollar helps boost the large cap multinationals even further. Nearly 40% of S&P 500 revenue resides offshore. A falling dollar makes our goods that much more attractive in other markets.

You have to be looking at the right market

I said earlier the markets are an important barometer of the economy, but you have to be looking at the right market. Investors have known for some time that fewer and fewer companies actually move the needle given the cap-weighted nature of the indices themselves. The top five by size — Apple, Amazon, Microsoft, Alphabet and Facebook — represent 23% of the S&P 500 and about 16% of the index's earnings.

S&P 500 (SPY) vs S&P 500 Equal Weight (RSP) vs Russell 2000 (IWM) Year to Date

The chart above compares exchange traded funds representing the S&P 500, the S&P 500 Equal Weight and the Russell 2000. Year to date, there's close to a 10% spread between SPY and the other two. The equal weight RSP and small cap IWM are a much better barometer of just where we are in the economic cycle.

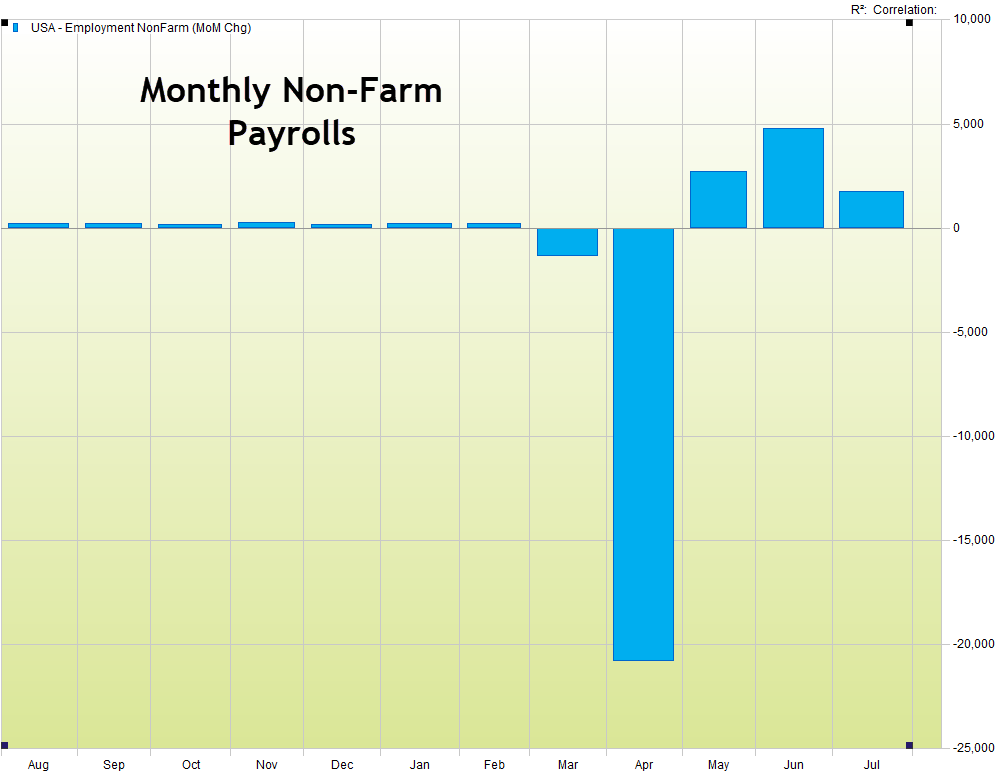

It's true we've added close to 9.3 million jobs in the last three months, but weekly unemployment claims are holding stubbornly above the 1 million mark. Democrats and the President are miles apart on the next round of stimulus, and the President's executive orders to extend relief to the millions off the payroll will clearly be challenged in the courts.

How about a little good news? So far this quarter, earnings reports are coming in way better than expected. They are still down an abysmal 34% from last year, but that's a lot better than the negative 44% analysts were forecasting.

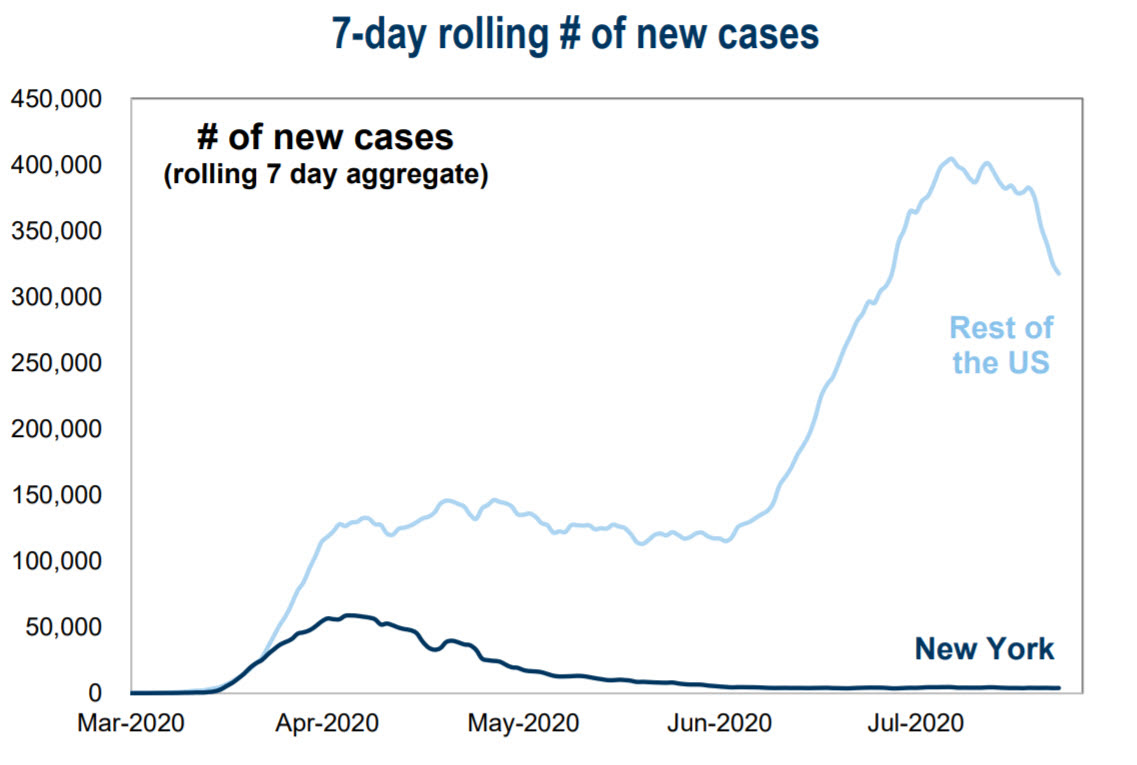

COVID-19 7-day moving average of new cases

There's even some good news in the fight against COVID-19. Nationally the 7-day moving average of new cases on a daily basis is starting to fall.

We're heading into a busy week as both Congress and the Administration go head to head over the President's executive orders, Joe Biden is expected to announce his running mate and finally we have no shortage of economic data and a continuing slate of earnings.

Happy trading!

Related: The Future of Pay TV Looks Very Different No

DISCLOSURE:The views and opinions expressed in this article are those of the contributor, and do not represent the views of Advisorpedia. Readers should not consider statements made by the contributor as formal recommendations and should consult their financial advisor before making any investment decisions. To read our full disclosure, please click here.