The BLS stunned investors Friday morning, reporting that the labor market was hotter than expected. The labor market added 353k jobs in January, almost double expectations for 180k. Furthermore, December’s figure was revised upward by 117k. Of some concern for the Fed, average hourly earnings grew by 0.6%, twice what was expected. However, there are inconsistencies with the data. For instance, hours worked fell by .2, and the labor market participation rate was 0.1% below expectations.

The biggest puzzle is the stark difference between the establishment and household surveys. The BLS establishment figure uses surveys of large companies to calculate the headline +353k number that is widely reported. The household survey gets its data from individuals. This data feeds the unemployment rate. The Household survey reported that the economy lost 31k jobs last month. The graph below shows the growing divergence between the two. In the previous two months, the household survey reported a loss of 714k jobs, while the establishment survey reported a gain of 686k. Per David Rosenberg, the Household survey diverged negatively from the establishment survey before each of the last four recessions.

Given that the BLS data is at odds with other labor indicators, including its own household survey, and that seasonal adjustments are big factors in December and January, we must be careful not to read too much into this round of labor market data.

What To Watch

Earnings

Economy

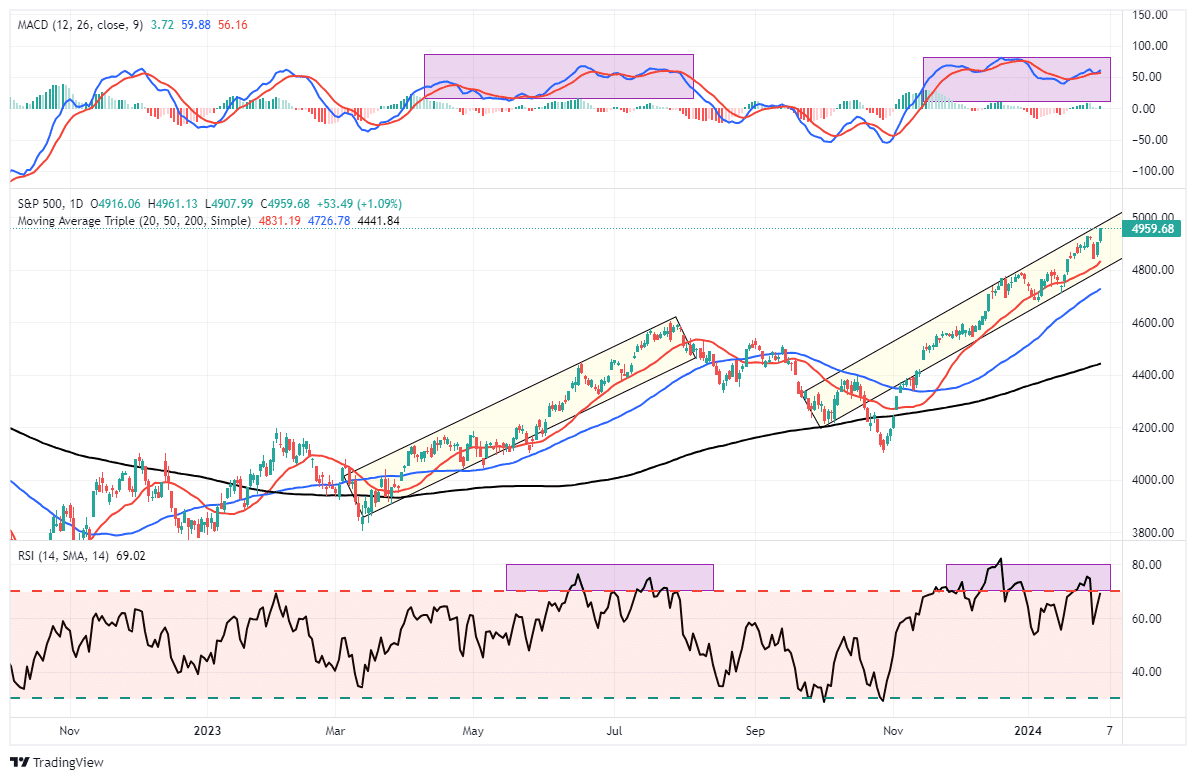

Market Trading Update

We have discussed the need for a market correction over the last few weeks. On Wednesday, the FOMC statement sent the stock lower as Jerome Powell eliminated the possibility of a rate cut by March. However, a stellar employment report on Friday, which would suggest the Fed stays on hold longer, sent the market surging to all-time highs.

While the media tried to apply several reasons why the market was higher, bullish momentum is intact. The selloff on Wednesday, as shown, tested the rising trend channel and opened a window for buyers to step in. There are only small windows of opportunity to increase equity exposure during substantial, bullish advances. However, as is always the case, the current “bullish stampede” will end, and a reversal will occur.

As shown above, the current bullish stampede is very similar to what we saw from March to July last year. At that time, it was the chase for “A.I.” that was driving the market while the majority of stocks dragged. The market remained overbought, trading in a defined trend channel as prices advanced. Then, the markets corrected by 10% into October, which is typical for any given year.

Today, we again see that same “unstoppable advance” with the same bifurcation in the market. While the “Magnificent 7” stocks again drive the markets, another 5-10% correction over the next several months should be no surprise. Such is particularly the case as we approach the upcoming Presidential election, where market participants may want to reduce exposure to offset potential election risks.

There is little reason to be overly concerned with the market for now. However, there is little doubt that the market is detached from the economic underpinnings. At some point, fundamentals will matter. But that isn’t today.

The Week Ahead

After a hectic week, markets will get a little break from the deluge of economic data and earnings announcements.

The bulk of fourth-quarter earnings are now behind us, with many prominent mega-cap names reporting last week.

Similarly, with the Fed meeting and employment data last week, there will be less for markets to cue on this week. We suspect Fed speakers will be out in droves refining the Fed’s position on potential rate cuts or tapering QT. Given Friday’s employment report, initial jobless claims will garner more attention. CPI, the following Tuesday, is the next big economic data point.

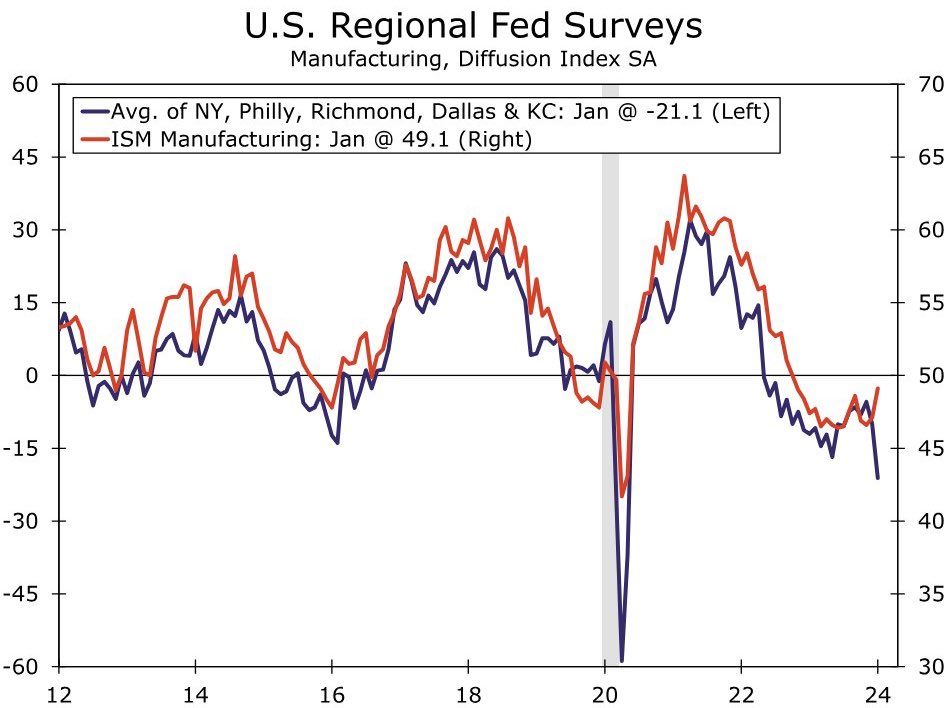

The Curious Case Of Manufacturing

Over the last couple of weeks, one regional Fed manufacturing report after another pointed to a deteriorating manufacturing sector. Consider the following:

- The New York Fed index fell sharply to its lowest level since May 2020. New Orders and shipments plummeted.

- The Philadelphia Fed index fell again and has been negative in 18 of the last 20 months. Both the current and future indexes point to economic contraction.

- Richmond’s Fed also reported a decline in its survey. It now stands at its lowest level since 2020.

- Per the Dallas Fed- “The production index, a key measure of state manufacturing conditions, dropped 17 points to -15.4—its lowest reading since mid-2020.”

- Like the other indexes, the Kansas City Fed also reported a contraction in manufacturing.

Given the poor surveys, we presumed the national ISM manufacturing survey would be similar. On Thursday, ISM surprisingly rose to 49.1%. While a reading below 50 signifies a manufacturing contraction, the index surprisingly was higher than the prior month. New orders, which hampered many of the regional indexes, rose from 47 to 52.5. Employment fell slightly and has been contracting for four months straight. The graph below shows the regional and national surveys correlate well. But, there are instances where they do diverge for a month or two. Stay tuned for the next round of surveys to see how the two data points converge.

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Related: The Pandemic Inflation Rollercoaster