The degree to which investors depend upon their financial advisor is changing, as more investors lean upon the advice of their advisor than in the past.

In its annual research into advisor usage among affluent investors, Spectrem’s 2020 study Evolving Investor Attitudes and Behaviors* found that the percentage of investors who are Advisor-Dependent, meaning they allow their advisor to make almost all decisions around investment strategies, was at 21 percent of all investors. That is a notable increase from the 13 percent who were Advisor-Dependent in 2009. The trend toward heavy advisor dependency has slowly increased over those 11 years.

At the same time, those who are Self-Directed investors, who use financial advisors minimally if at all, has also increased, up to 39 percent in 2020 from 32 percent in 2009.

That response is an unusual one; either investors are going all in with their advisor, or they are avoiding advisor use all together. Only 41 percent now sit in the middle section, either Advisor-Assisted (using an advisor to provide guidance on all investments but making their own decisions) or Event-Driven (using an advisor for special purposes such as retirement planning or education funding plans). In 2009, 55 percent were in those two middle segments of advisor dependency.

When examining advisor dependency by wealth, the wealthier the investor, the more likely they are to be Advisor-Dependent, up to 25 percent for those with a net worth between $15 million and $25 million. However, that same wealth segment has one of the higher Self-Directed percentages, 42 percent, compared to 30 percent of those with a net worth between $3 million and $5 million.

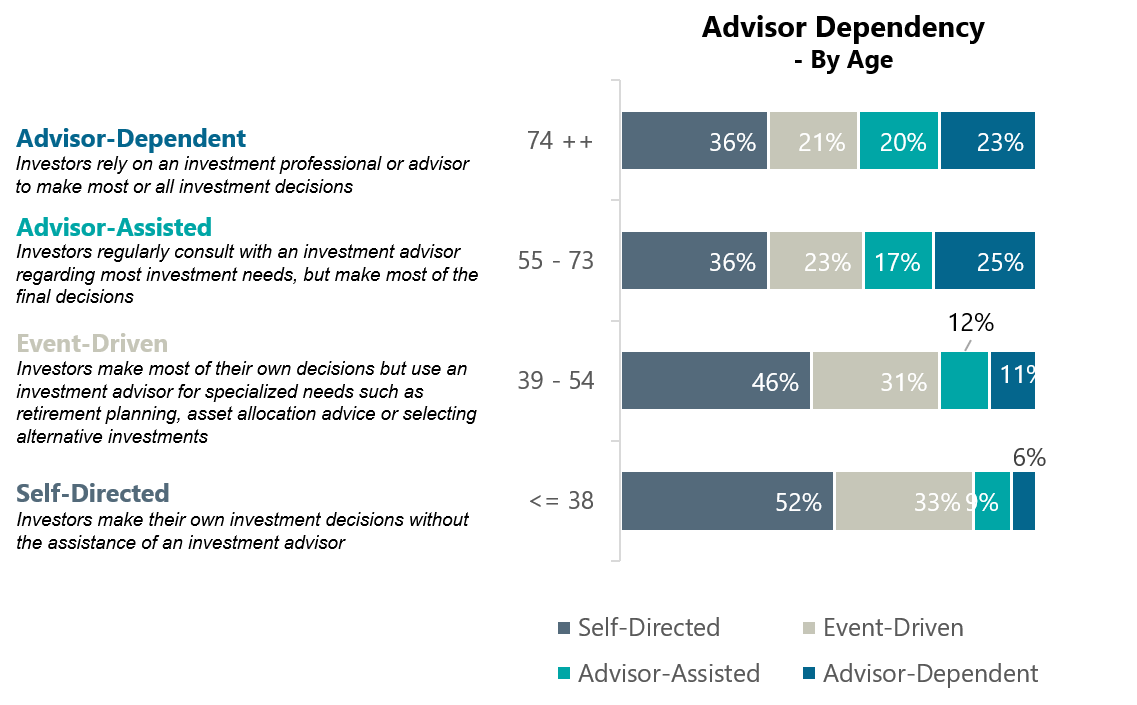

There is also a huge difference in advisor dependency based on age. Fifty-two percent of Millennials are Self-Directed investors and only 6 percent claim to be Advisor-Dependent. On the other end of the spectrum, 23 percent of World War II investors are Advisor-Dependent and only 36 percent are Self-Directed.

For advisors, Millennials are a target to alter their use of financial professionals. As their personal finances get more complicated with children and college planning and the closer thought of retirement, their use of financial advisors is likely to change. Providing an opportunity to consider the benefits of advisor usage is a way to entice Millennials to accept such services.

Related: Investors Who Do Not Use Advisors