Some time periods are more telling than others. But it’s a moving target.

You see it at the bottom of every investment product advertisement that includes performance information: “Past performance is no indication of future returns.” As someone who analyzed portfolio performance for a living before I switched to the other side of the table and became the portfolio manager, I agree with that. However, I only agree with it up to a point.

You see, investment performance is probably the most misunderstood facet of investing. The world seems to be divided into a few camps:

- Those who spin past performance so that it has a lot of sales value, but leaves out critical information. This is common, and it is what eventually produces investor frustration, particularly with the financial advice industry.

- Those who get fixated on “standard” past performance time frames. They “keep score” year to year, year-to-date, 5 years or 10 years. There has been so much standardization as the world became wealthier (since the early 1980s), I wonder if the mainstream will ever be able to correct some of the dangerous flaws in this. As an example, think about what you see from your 401(k) plan at work. Typically, the investment choices contain the name of the investment, the investment category, and some standard past performance periods. That’s some rigorous analysis there…not!

- Those who see past performance as a way to extract some very meaningful data to help investors truly understand what their portfolio or individual investments are really capable of. That involves looking more at “rolling” time periods rather than simply analyzing static periods. Count me as being firmly in that camp.

Today’s feature: your portfolio’s performance!

It is like going to the movies (as we used to do, and will again!). If you walked into the wrong theater by accident, and saw 2 seconds of a movie, you might be tempted to judge whether you would see that film another time. That’s what analyzing a static time period can be like if you are not careful. To judge a movie, you need to watch all of it, or at least most of it.

The limits of this column prevent me from pouring out tons of performance data on a variety of securities and investment approaches (you are welcome!). However, I have provided 2 snapshots below at static time periods that should matter more to you than the standard ones in judging how you have done, and developing expectations for the future.

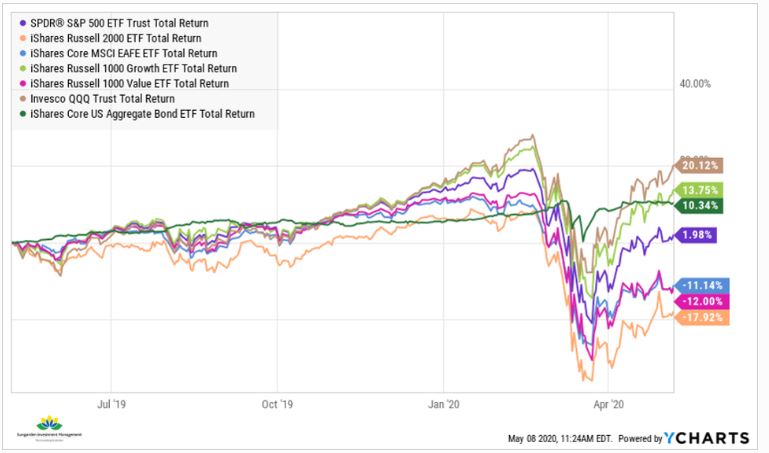

The past 12 months have been a better-than-average period to evaluate

There is a lot of “spaghetti” in that chart below, so allow me to summarize for you. In the past 12 months (5/8/2019 – 5/7/2020), the “headline” stock market index, the S&P 500, rose sharply, then plunged at record speed, then bounced back up. At the end of the 12 months, it was about 2% above where it was last year.

Some will say this is a victory. I say it looks like what happens in bear markets. Either way, we can use this information to size up how we balance reward and risk of major loss. After all, that’s what retirement investing is, in its most simplistic form.

As I have written for a couple of years now, the bullish (up) investment cycle for stocks was in its latter stages. That helped the S&P 500 mask weakness in other parts of the market. For instance, as the chart above shows, the Nasdaq 100 NDAQ was up over 20% during the past 12 months.

US Large Cap Growth stocks did very well, too. Non-U.S. stocks and US Large Cap Value stocks did very poorly. And Smaller Stocks were down 18%, or 20% behind the S&P 500. This pattern has been going on for a while.

“Stocks, shmocks.” Here is what really stood out.

Perhaps most importantly, the US Aggregate Bond market rose 10% during the period. This accompanied a “crash” in interest rates, that turned bond prices higher. This is the only reason why “Balanced” portfolios don’t look much worse than they do. But this type of return for bonds is likely not sustainable. The math is against it, with interest rates so low.

And, just recognizing that fact can help you understand that this particular 12-month period was pretty revealing. What did it reveal? This all adds up to one thing: a very narrow market, where a small number of stocks carry the rest. In your own portfolio, it could go a long way toward explaining how you performed the past 12 months.

As I see it, this type of whipsaw action, even in the S&P 500, is the type of thing investors have not had to deal with for about a decade. That prompts some re-education. And yes, I have volunteered for that job.

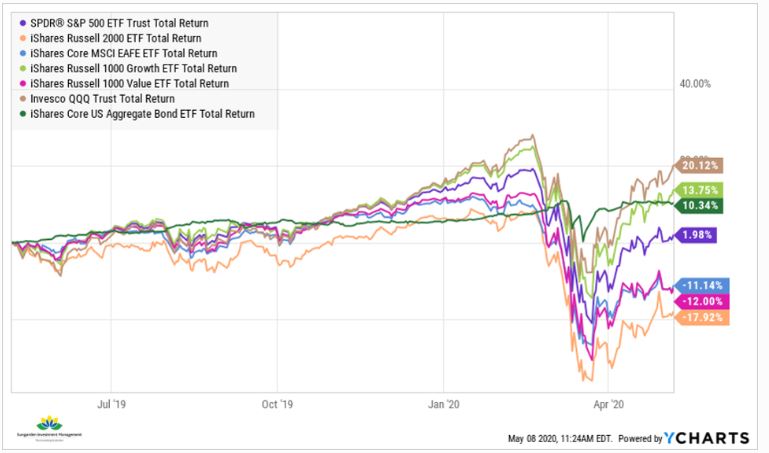

Analyzing performance from major market turning points can be very helpful.

Above you see one more time period. This one starts on 10/3/2018. That’s when the stock market initially topped out. It then cratered for all of 3 weeks, rebounded on Christmas Eve, 2018, and flew higher until this past February.

In market cycle language, we call that the “melt-up” phase. It is the last one in the cycle before volatility takes over. At that point, the rules of earning returns from stocks (and now bonds as well) shift dramatically. I think that’s where we are now.

What a bear market looks like

That graph is showing a period of about 19 months. Notice that many of the market segments on the chart produced similar returns over these 19 months than they did over the 12-month chart I showed you earlier. In other words, we have had a 7-month roller coaster that produced a near-zero S&P 500 return. Then, we had a 12-month return that produced…essentially the same thing. Welcome to bear market investing.

Bottom-line: investing is different now. It is not more difficult, if you look beyond the “headlines” of standard marking periods for your portfolio. Bear markets are not about “set it and forget it.” They are about recognizing that there will be some big “ups” and some big “downs” and they may cancel each other out. This can go on for years.

Most recently, the S&P 500 was roughly flat from 1999-2009. Then, as now, there is a constant opportunity for those who play offense and defense, and prioritize flexibility in their portfolio management.