Tens of millions of retirees are facing a retirement financing crisis. They saved too little, retired too early, took Social Security too early, and will die well beyond their expiration dates. Many had no access to employer-provided retirement plans. Others chose not to participate or contributed less than the max. Yet others participated fully and then sat back, confident their employers and Uncle Sam would secure their retirements. They were praying, not planning.

How about private pensions? Corporate America swindled private-sector workers out of those decades ago. As for union, state, and local pensions, many are effectively insolvent when you properly discount their obligations/liabilities — using the term-structure of TIPS — Treasury Inflation Projected Securities (bonds) not the miles higher average return on highly risky equities, which these pension systems’ “fiduciaries” routinely use to disguise their systems’ financial shortfalls.

Social Security is also broke, indeed dead broke. The System is a colossal $65.9 trillion in the red. The System’s funding problem is short as well as long term. A decade from now, the Agency will run short on cash, triggering a 20 percent benefit cut. As for private savings, two in five retirees have none. Most with savings also have debts, leaving them with net wealth sufficient to cover only a few years of spending.

One saving grace is Baby Boomers’ home equity, estimated at a massive $18 trillion. But tapping home equity comes at a price. Let me expand on a case study I provided Neal Templin — Barron’s terrific editor and writer. Neal covered the example in his recent article, How to Determine if Renting or Owning is Right for You. I constructed the illustration using MaxiFi Planner, my company’s economics-based lifetime personal financial planning software.

Meet the Swansons — Members of the Top 1%

The example features a hypothetical 65 year-old retired couple — Jim and Gloria Swanson — who own a $2 million condo, albeit with a $500K mortgage, in the expensive Boston Seaport area. In the old days, it was Whitey Bulger’s dumping ground for his victims. But, of late, it’s the tony place to be.

Jim and Gloria think themselves quite well off given their expensive pad (with its doorman) and their $2 million in IRAs. But that money is taxable on withdrawal. Also, property taxes, condo fees, insurance, and maintenance are costing them over $30K a year. Then there’s Mass income taxes, Medicare’s Part B IRMAA premiums, and federal income taxes.

How Rich Is this “Rich” Household?

The answer is not very. As you can see from MaxiFi’s chart below, well over half of the couple’s remaining lifetime resources are going out the window to cover fixed expenses, specifically, taxes, including Medicare premiums, and housing costs. This leaves the couple with $5K each month to spend on discretionary items. Note. The plan assumes Jim and Gloria earn 2 percent above inflation by investing in the safest asset around, namely TIPS — Treasury Inflation Indexed Bonds.

The rub is that Jim and Gloria are foodies. Their life resolves around trying a new restaurant every night and arguing the next day over its quality. This habit averages $100 per meal leaving them with $67 a day to spend on everything else. After adding up their morning visits to Starbucks, gifts for the grandkids, gas and repairs on their Mercedes, toilet tissue, tipping the doorman, donations to NPR, the Boston MFA, and …, well, light dawns on Marble Head. (This is, as I’ve previously noted, my favorite old New England saying. Marble Head is a beautiful town on Boston’s North Shore.)

Jim and Gloria, to their extreme consternation, realize that even millionaires, as they proudly call themselves, can be left counting pennies.

How Much Is their Housing Really Costing?

The next chart from MaxiFi details the couple’s lifetime budget, including their spending, measured in present value, on housing. The couple is allocating $3.1 mil of their $5.3 mil of lifetime resources on housing. Thus, they are spending roughy $2 on housing for $1 spent on everything else. The $3.1 mil breaks down into $1.1 mil in direct expenses, $1.0 mil in trapped equity, and almost $1.0 mil in housing holding costs.

Housing expenses encompasses mortgage payments, property taxes, condo fees, insurance, and maintenance. Trapped equity is the present value of the condo net of any remaining mortgage, which they’ll bequeath at the end of their days — assuming, as they do, that they will both die in place. As for housing holding costs, it references the loss of real interest the couple could otherwise be earning on their $2 mil housing investment.

Meeting with a Financial Planner

Jim and Gloria are starting to panic. So, they schedule a meeting with a financial advisor named Megan. Megan tells them they should move their IRAs out of TIPS and into her “safe” equity fund where she’s been averaging 9 percent real. Safe, as Megan tells the couple, means being able to meet their spending “needs” with an 80 percent probability.

Sounds pretty good, no? Actually, it sounds terrible. Megan is proposing leaving the Swansons with a 20 percent chance of losing their $2 million IRA assets in its entirety. Megan is eager to sign them up at a $20,000 asset-management fee per year. She assures them that “stocks are safe over time.”

But Jim and Gloria aren’t buying Megan’s pitch. They don’t view losing all their IRA assets one fifth of the time, possibly even this year, as “safe.” They view it as nuts. Indeed, they wonder, as do I, whether conventional planning’s classifying an investment strategy with an 80 percent chance of success as safe violates a reasonable fiduciary standard. Even a 5 percent chance of losing all of one’s financial asset, let alone a 20 percent chance, is not something any decent economist would endorse.

Un-Trapping their Trapped Equity

Jim and Gloria politely tell Megan that she should take a course in finance at a top economics department or business school — where conventional planning doesn’t appear on the syllabus. Next, they run MaxiFi and see what the they’ve come to realize — the couple is so house rich that it’s house poor.

But, Jim and Gloria aren’t ready to give up their evening repays. They love their kids and realize that literally eating up their “trapped equity” will mean leaving the kids with nothing but the car. On the other hand, a lot of their gains will come from being able to invest the proceeds of the sale of their condo.

“Well, too bad for the kids. Let them fend for themselves.” is their conclusion. So, they form a plan. Sell their condo, but rent their neighbor’s identical unit for $5000 a month.

Here’s MaxiFi’s good news. The couple can now spend an extra $16,694 a year or $1,391 a month. The bad news is that this will only cover 14 days a month of their foodie excursions. But if they focus on restaurants with large portions, they can eat their meals twice — once in real time and once as leftovers.

Getting Real

After contemplating their new plan, Jim and Gloria realize they still won’t be able to make ends meet. Yes, they are now spending $1.6 mil, over their remainders, on housing — less than their now higher $2.0 mil in present value spending. But they’ll still spend beyond their means even eating leftovers. In the end, Jim and Gloria do what half their friends have done. They sell their homes that are making them poor and move to, that epicurean delight — the Volunteer State, i.e., Tennessee. (TN got its nickname by sending volunteers to fight in the War of 1812.) Jim and Gloria decide to purchase a $650K 2,200 sq ft 3 bedroom, recently built home in Nashville. Here’s the picture of the one I found for them on Zillow.

Rescuing the Swansons’ Retirement — Moving to Tennessee

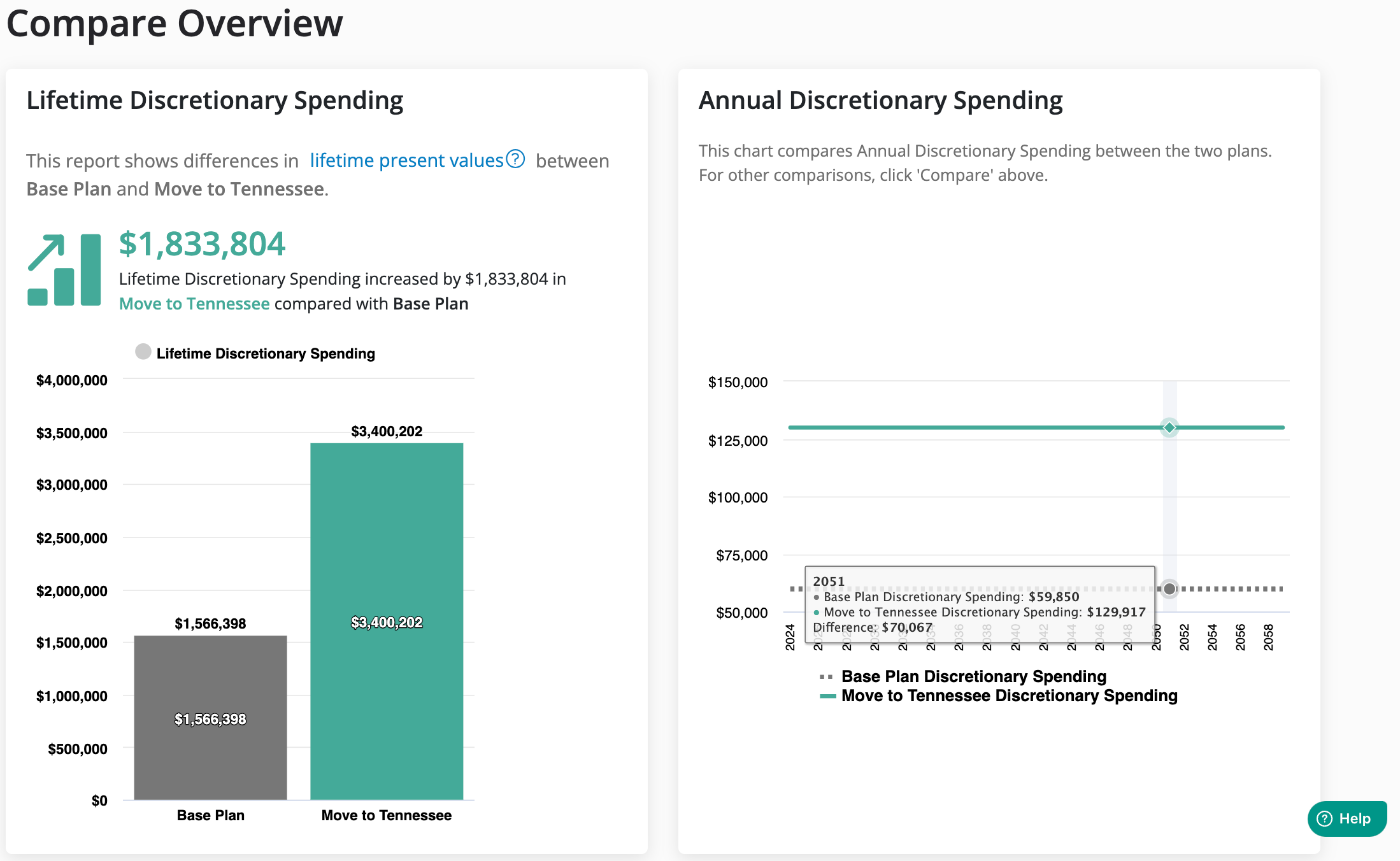

Jim and Gloria set up a new profile in MaxiFi in which they sell their Boston condo, buy the above-pictured house in TN and dramatically lower their housing costs compared with either continuing to own or rent in the Seaport. The program takes a half second to show why this move rescues their retirement. As MaxiFi’s profile comparison chart, shown below, makes clear, this entirely safe move more than doubles the couple’s lifetime discretionary spending. The increase is a whopping $1.8 million! And the couple’s annual discretionary spending rises by $70,067! That more than four times the increase from selling and renting in the Seaport. Part of the gain, by the way, reflects reduces state income taxes. TN, like eight other U.S. states, doesn’t have an income tax. In their case, Jim and Gloria save $93K in remaining lifetime Mass state income taxes. Jim and Gloria also like this new plan because it leaves their kids with a house, albeit a third as valuable. Their kids are happy too. They realize that on their current path, dad and mom are going to need a major financial bailout down the road, which will fall in their laps.

As for eating BBQ and not eating veggies? Truth be told, Jim was playing foodie to make Gloria happy and Gloria was doing it to make Jim happy.

Bottom Line

If you aren’t running MaxiFi to make your financial decisions, you are surely leaving a ton of safe money on the table. Whether it’s deciding when to retire, how to pay off your student loans, which career to follow, whether to switch jobs, perhaps in a different city with a different salary and 401(k) plan, how to invest, or whether you can afford to get divorced, MaxiFi can provide real guidance.

If you don’t like running software on your own, you can purchase our co-piloting service with the fabulous PhD economist and CFP, Jay Abolofia, or plan with me. In that case, I’ll do all the work and give you a fully loaded (with your data) version of MaxiFi for free. And if you are one of the thousands of DYIers who are running MaxiFi, Dan Royer, our fantastic head of MaxiFi customer support, will answer your standard questions for free. But he’ll also review your inputs and outputs with you for a small fee.

Finally, if you are working with an advisor, ask them to run your plan through MaxiFi Planner PRO. They’ll see the enormous difference between using advanced software and conventional hyper-risky planning based on 70-year-old rules of thumb.

Related: Why Today's Housing Market Is Crazy